Overview

Entities within Queensland's education sector aim to help individuals make positive transitions from early childhood through all stages of schooling, providing the knowledge and skills to prepare them for future education, training, or the workforce.

The education sector, for the purposes of this report, includes the Department of Education; the Department of Employment, Small Business and Training; TAFE Queensland; seven universities; eight grammar schools; and some other statutory bodies.

Tabled 27 May 2021.

Report on a page

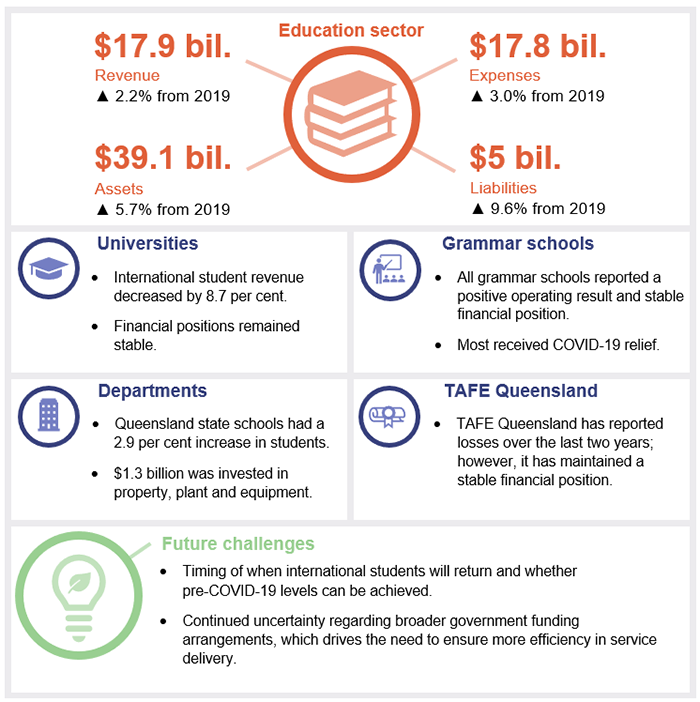

This report summarises the audit results of entities in Queensland’s education sector, including the Department of Education; the Department of Employment, Small Business and Training; TAFE Queensland; seven universities; eight grammar schools; and some other statutory bodies.

Financial statements are reliable

The financial statements of all education entities are reliable and comply with relevant reporting requirements. Entities have mature financial statement processes and were able to prepare good quality financial statements, despite the challenges presented by the pandemic.

Entities reacted quickly to risks from COVID-19

International border closures resulting from COVID-19 had a significant impact on universities. This year, revenue from international students decreased by $134 million (nearly nine per cent of total international student revenue). Universities responded quickly to reduce costs.

Grammar schools received assistance through federally funded COVID-19 assistance programs to support their financial results this year. They will need to reassess the cost of their services as government assistance reduces.

State schools adopted new technology to support remote learning for the five weeks of COVID‑19 lockdown, and made alternate learning resources available for students with limited or no access to computers and/or the internet. The Department of Education is reviewing its response to the pandemic to develop approaches for using technology to deliver learning in the future.

Entities need to cope with funding uncertainty

Across the sector, future revenue streams remain uncertain. In order to remain viable, all entities need to understand the cost of delivering their services over the medium and longer term and monitor the efficiency of their service delivery.

Asset management is essential for future planning

Education entities invest significant funds in maintaining, replacing or upgrading assets. It is important this is done at the most cost-effective point in an asset’s life. Entities need a good understanding of the condition of their assets and future demand for their services to plan for effective asset management. To meet forecast demand and reduce pressure on existing schools, the Department of Education is building schools in regions with strong population growth. This investment needs to be integrated with its digital strategy.

Strong information systems are critical

While we were able to rely on entities’ systems and processes used to prepare financial statements, we identified some deficiencies. Security of information systems continues to be the area where we find the most issues.

Given the sensitive nature of information held about students and research, education entities are an attractive target for cyber attacks. They must update their systems promptly to respond to changes within their entity and to remain vigilant from external threats.

Recommendations for entities

We have identified the following recommendations:

Strengthen the security of information systems (all entities) |

|

|

All entities should strengthen the security of their information systems. They rely heavily on technology, and increasingly, they must be prepared for cyber attacks. Any unauthorised access could result in fraud or error, and significant reputational damage. Their workplace culture, through their people and processes, must emphasise strong security practices to provide a foundation for the security of information systems. These practices must also be cognisant of other users, such as students, to ensure that all networks are as secure as possible. Entities should:

Entities should also self-assess against all of the recommendations in Managing cyber security risks (Report 3: 2019–20) to ensure their systems are appropriately secured. |

|

Understand the cost of service delivery to make informed decisions about future services and efficiencies in operations (education entities) |

|

|

In order to remain sustainable in the longer term, education entities need to continue to develop their understanding of the value of their services and the cost of delivering them. They should use this understanding to decide whether to offer the same services in the future or invest in others that are more efficient or of greater value to customers. |

|

Improve asset condition assessments (all entities) |

|

| REC 3 |

All entities need to regularly review the condition of their assets to ensure they understand current and future maintenance requirements. Entities need to use accurate information about the condition of their assets to inform their long-term asset management strategies, which should consider both physical assets and digital infrastructure. |

Reference to comments

In accordance with s.64 of the Auditor-General Act 2009, we provided a copy of this report to relevant entities. In reaching our conclusions, we considered their views and represented them to the extent we deemed relevant and warranted. Any formal responses from the entities are at Appendix A.

1. Overview of entities in this sector

This report summarises our financial audit results for education sector entities as at their year‑end dates for preparing financial statements. For the Department of Education; the Department of Employment, Small Business and Training; TAFE Queensland; and some statutory bodies, this was 30 June 2020. For universities, grammar schools, and other statutory bodies, it was 31 December 2020.

We provide 40 opinions in this sector. The analysis in this report focuses on the 18 entities highlighted in Figure 1A, representing 99.2 per cent of revenue within the education sector.

Note: Yellow outer circles indicate the entities included in this report.

DoE—Department of Education; DESBT—Department of Employment, Small Business and Training; TAFEQ—TAFE Queensland; CQU—Central Queensland University; UQ—The University of Queensland; QUT—Queensland University of Technology; GU—Griffith University; USQ—University of Southern Queensland; JCU—James Cook University; USC—University of the Sunshine Coast.

Queensland Audit Office.

2. Results of our audits

This chapter provides an overview of our audit opinions for entities in the education sector and of the effectiveness of the systems and processes (internal controls) they use to prepare financial statements.

Chapter snapshot

Audit opinion results

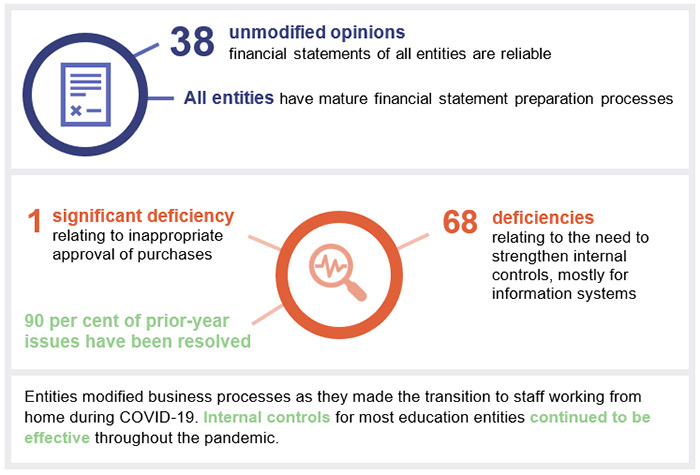

We issued unmodified audit opinions for all education entities in Queensland, within their legislative deadlines. Readers can rely on the results in the audited financial statements. The details are provided in Appendix C.

We express an unmodified opinion when financial statements are prepared in accordance with the relevant legislative requirements and Australian accounting standards.

Entities not preparing financial statements

Not all Queensland public sector education entities produce financial statements. The full list of entities not preparing financial statements and the reasons are provided in Appendix D.

Education entities self-assessed their financial statement preparation processes as mature

Most education entities have established financial statement preparation processes that are appropriate for their size and complexity. These processes meant they did well this year to prepare good quality financial statements on time, given the challenges arising from the COVID‑19 pandemic.

In 2019, universities were the first to undertake a self-assessment of their financial statement preparation processes, using the maturity model on our website. This year, we worked with the departments, TAFE Queensland, and the grammar schools as they performed self‑assessments.

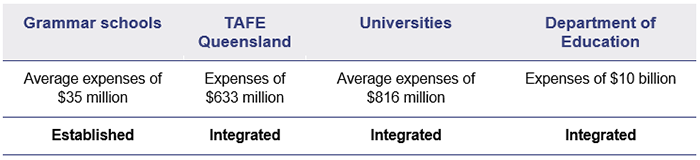

Figure 2A shows that the average maturity of financial statement preparation processes increases with the size of the education entity. Grammar schools have smaller and less complex operations than most other education entities. We would not expect them to invest in maturing their financial statement preparation processes unless they have assessed there to be a real benefit in efficiency or quality.

Notes: Established—third highest level of maturity. Integrated—second highest level of maturity.

Queensland Audit Office.

The Department of Employment, Small Business and Training’s maturity was assessed as established this year. While this is a larger entity, its financial statement preparation processes are still developing after the department was created on 12 December 2017.

Strengths identified across the sector included good quality proforma statements (financial statements prepared before year end that focus on wording and structure) and month‑end financial reporting processes. These proved to be of significant benefit given the additional pressure on finance teams as a result of the COVID-19 pandemic—which included working from home and implementing cost-saving measures.

Larger entities have recognised the importance of continually refining their financial statements so they reflect the most significant aspects of their operations and meet the needs of users. This includes clearly explaining the complex assumptions and estimates they apply in their financial statements. This will continue to be a focus in coming years.

Larger entities are also looking for further opportunities to automate aspects of their monthly processes. These measures will continue to improve the efficiency and quality of their financial statement preparation.

Internal controls are generally effective

In 2019–20, we found the internal controls education entities have in place to ensure reliable financial reporting are generally effective. While we were able to rely on them, we identified one significant deficiency (a high-risk issue) in internal controls, as payments had been authorised by an employee who did not have the financial delegation to do so. We performed additional testing to conclude that this had not resulted in a misstatement in the financial statements.

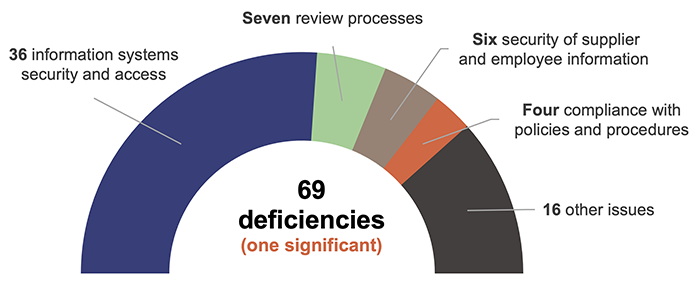

Figure 2B shows the nature of internal control deficiencies reported during the year.

Queensland Audit Office.

The majority of education sector entities have either addressed their identified control deficiencies or are on track to do so by the agreed dates. Proactive and timely resolution of deficiencies indicates a strong foundation for the effective operation of internal controls.

Security of information systems continues to be the most common control weakness

Most deficiencies identified during the year related to information systems, including:

- insufficient monitoring of the access and activities of privileged users (who have access to sensitive data and can modify information)

- ineffective management of user access to systems

- poor password practices for networks and applications.

Weaknesses over controls in information systems increase the risk of undetected errors or potential financial loss, including from fraud. Our report to parliament—State entities 2020 (Report 13: 2020–21)—identified a significant increase in cyber attacks and phishing attempts (scams that trick people into providing confidential information through email or message platforms) since the start of the pandemic. Education entities are popular targets for cyber attacks given the nature of the information held about students and research materials. Their information systems are further complicated by their need to share information with other users (both students and research collaborators). In order to maintain a strong information security environment, entities need to consider all users of their systems.

All entities need their people and processes to demonstrate strong security practices so their information systems are promptly updated, they can respond to changes within their entity, and they can protect against external threats.

Recommendation for all entitiesStrengthen the security of information systems (REC 1) |

|

All entities should strengthen the security of their information systems. They rely heavily on technology, and increasingly, they must be prepared for cyber attacks. Any unauthorised access could result in fraud or error, and significant reputational damage. Their workplace culture, through their people and processes, must emphasise strong security practices to provide a foundation for the security of information systems. These practices must also be cognisant of other users, such as students, to ensure that all networks are as secure as possible. Entities should:

Entities should also self-assess against all of the recommendations in Managing cyber security risks (Report 3: 2019–20) to ensure their systems are appropriately secured. |

Processes were adapted in the transition to working from home

Most entities made the transition to staff working from home in March 2020 to comply with COVID-19 restrictions and support social distancing. As restrictions ease, we are now seeing a combination of staff working from home and in the office.

The transition to the new working arrangements resulted in most entities modifying business processes so they could be performed remotely, investing in computer hardware, and implementing secure technologies to facilitate remote access. This meant they were able to maintain business-as-usual practices during the pandemic.

These changes in working arrangements have increased the risk of controls failing, due to changes in manual business processes (including relying more on technology—for example, allowing remote access and using electronic signatures) and the reduced capacity for supervision.

We identified seven instances where reviews of journals (used to record transactions that do not involve cash), monthly reconciliations (such as matching the cash at bank to accounting records), and reporting (to monitor whether processes are occurring) were either not performed or were not performed in a timely manner.

Despite this, our audits found internal controls for education entities have generally operated effectively throughout the pandemic and were able to be relied on when preparing financial statements.

3. Financial challenges faced by education sector entities

This chapter analyses the financial performance and position of the 18 education sector entities, and the challenges faced by the sector.

Chapter snapshot

Universities have responded to risks from COVID-19

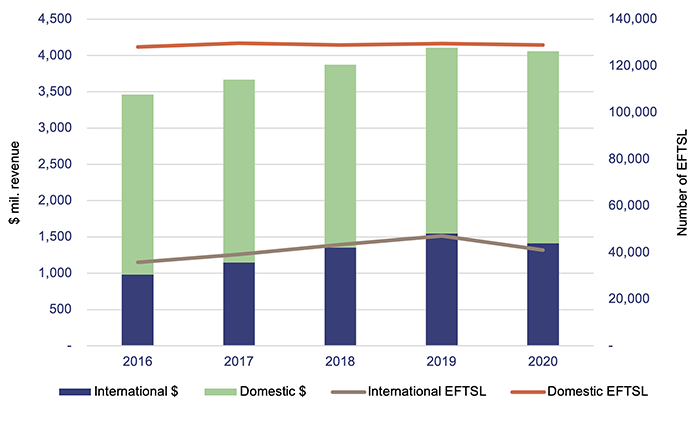

Universities have increased their reliance on revenue from international students in the last five years, in response to changes to Australian Government funding and increased competition in the domestic student market.

In 2020, total revenue recorded by the university sector from international students decreased by 8.7 per cent due to the impact of COVID-19. While the sector was affected by international border closures, the full impact was mitigated in 2020 as some students enrolled in courses were in the country when travel restrictions came into effect. Universities were also able to offer online learning and provided fee assistance to support international students to continue their studies.

Note: Not all students study full-time for a whole year. Equivalent full-time student load (EFTSL) is a way of representing the various study loads as a proportion of the study load the students would have if studying full-time for one year. ‘Number of EFTSL’ adds all of these together.

Queensland Audit Office.

Actions taken by all universities to manage COVID-19

Universities responded quickly to the COVID-19 pandemic throughout 2020 to minimise the decline in their revenue and reduce expenses. Their actions included:

- moving to online learning—With campuses closed to students from March 2020, all universities moved to digital delivery of courses. This also enabled them to retain some of their off-shore international students who continued their studies despite not being in the country

- restructuring—Each university has begun restructuring to better position itself for the medium and longer term. This has included early retirement and redundancy programs, as well as reviews of strategic direction

- assessing expenses—All universities reduced operating expenses, largely related to commissions paid to agents (who help recruit international students), travel, and discretionary spend (for example, for events and hospitality). All universities also reviewed their planned asset purchases and maintenance programs, and some deferred activities to future years.

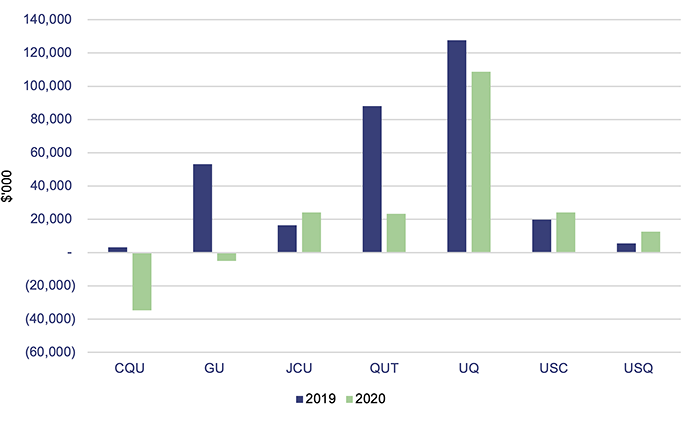

Their 2020 results confirm these actions have been effective in the short term.

Note: CQU—Central Queensland University; GU—Griffith University; JCU—James Cook University; QUT—Queensland University of Technology; UQ—The University of Queensland; USC—University of the Sunshine Coast; USQ—University of Southern Queensland.

Queensland Audit Office.

Prior to 2020, Central Queensland University had the highest reliance on international course fees, which made up 36 per cent of its total revenue. This meant it was the hardest hit when the pandemic caused border closures and restrictions on travel. The university incurred an operating loss of $34 million (2019: profit of $3 million). International student revenue decreased by $54 million but was offset by increases from other revenue sources, including from domestic students, resulting in an overall decrease in revenue of $37 million.

Central Queensland University took decisive action and was the first university to undertake an organisational restructure, resulting in 296 staff separations. It entered into new financing arrangements, which included a $20 million Queensland Treasury Corporation overdraft facility (not accessed as at 31 December 2020) and a $70 million loan from the Australian Government for its asset purchases, with $35 million received in December 2020 and the remainder expected to be used in 2021. It permanently closed its campuses at Biloela, Yeppoon, and Noosa.

Outside of COVID-19 impacts, the significant decreases in operating results for Griffith University and the Queensland University of Technology were largely due to lower investment income of $7.2 million in 2020 compared with $111.5 million in the prior year. This movement represents changes in the value of investments they hold and does not impact their cash balances. Investment income is dependent on market conditions.

Continued uncertainty for universities

The effects of COVID-19 are expected to continue well into 2021 and beyond for the university cohort. Due to the lower international enrolments this year, most universities are budgeting for lower revenue in the short term. The impact of this has been partially offset by increased domestic enrolments.

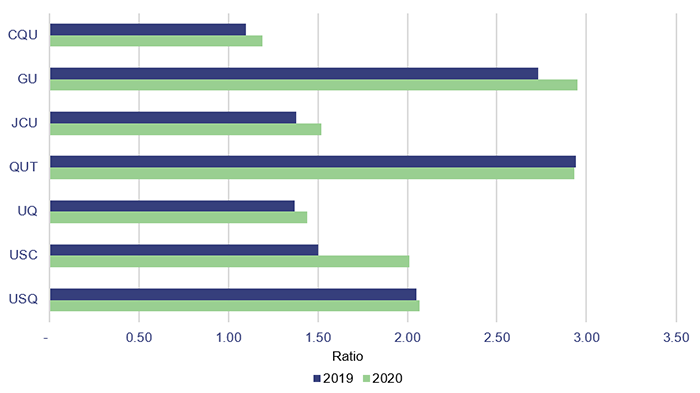

Figure 3C shows the universities’ ability to pay their debts as and when they fall due, where we compared their liquid assets (cash and investments) to the liabilities they expect to pay over the next 12 months. A ratio of less than one indicates that a university may face some short-term challenges in supporting its ongoing operations.

Note: CQU—Central Queensland University; GU—Griffith University; JCU—James Cook University; QUT—Queensland University of Technology; UQ—The University of Queensland; USC—University of the Sunshine Coast; USQ—University of Southern Queensland.

Queensland Audit Office.

In the longer term, universities will continue to face significant risks with the security of their funding. Four universities have budgeted for a loss in 2021. All universities are expecting lower international student enrolments, which will impact their revenue for at least three years (being the minimum for a degree).

At the time of preparing budgets, most of the sector anticipated that international students would be able to return sometime in 2021. The universities’ ability to attract and retain students at pre‑COVID levels remains unknown. A secondary impact is that the delivery of courses is likely to change given some were able to be fully online this year. This is likely to increase competition for international students globally as it removes some barriers, including visas.

Also, several changes have been made to Australian Government funding in recent years, with the introduction of new funding packages being implemented in 2021. Universities are still determining the impact these changes will have on their long-term outlooks.

To address the ongoing uncertainty, universities will need a clear understanding of what they will deliver in a post-pandemic environment. As the demand may be different to current expectations, they will need to ensure they deliver their courses and services in an efficient and flexible manner, while also achieving their strategic objectives.

Recommendation for all education entitiesUnderstand the cost of service delivery to make informed decisions about future services and efficiencies in operations (REC 2) |

|

In order to remain sustainable in the longer term, education entities need to continue to develop their understanding of the value of their services and the cost of delivering them. They should use this understanding to decide whether to offer the same services in the future or invest in others that are more efficient or of greater value to customers. |

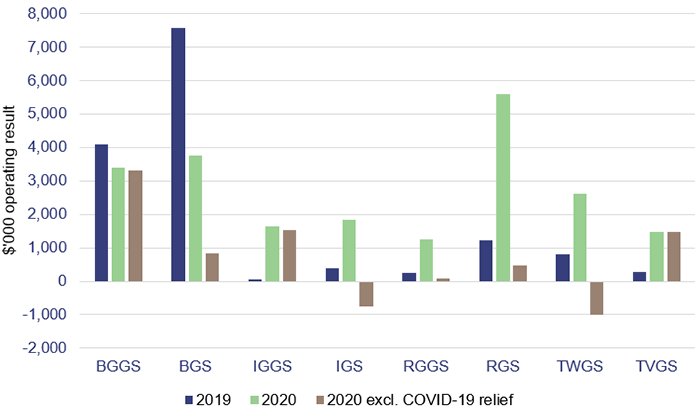

Grammar schools received support during COVID-19

Six out of eight grammar schools increased their operating result in 2020, and all grammar schools increased their total revenue. However, significant Commonwealth COVID-19 relief payments were received by five out of eight grammar schools during this time. Brisbane Girls Grammar School, Ipswich Girls’ Grammar School and Townsville Grammar School did not receive significant Commonwealth COVID-19 relief payments.

Figure 3D shows that when the COVID-19 relief is excluded, the operating result for six out of eight grammar schools declined.

Note: BGGS—Brisbane Girls Grammar School; BGS—Brisbane Grammar School; IGGS—Ipswich Girls’ Grammar School; IGS—Ipswich Grammar School; RGGS—Rockhampton Girls Grammar School; RGS—Rockhampton Grammar School; TWGS—Toowoomba Grammar School; TVGS—Townsville Grammar School.

Queensland Audit Office.

Expenses for the grammar schools grew consistently with prior years, however revenue has not grown at the same rate. Revenue was impacted by the COVID-19 restrictions with an overall decrease in boarding fees of $2.9 million. Should this prove to be a longer-term trend driven by economic conditions, grammar schools will need to look for efficiencies within their operations.

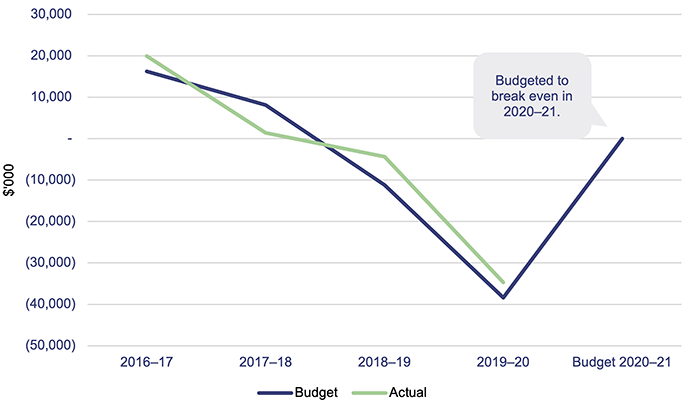

TAFE Queensland incurred a second year of losses

TAFE Queensland has been experiencing declining profits and recorded an operating loss for the second consecutive year in 2019–20. While training revenues increased from the previous year, overall revenues were lower due to changes in funding arrangements with the Queensland Government, and increases in employee costs under enterprise bargaining agreements. In addition, it has to meet the Queensland Government’s service expectations to provide quality training in remote and regional areas or where there is low demand, while operating in a contestable market. This poses significant financial challenges.

TAFE Queensland performed slightly better than its budgeted loss in 2019–20, which was set prior to COVID-19. The postponement of face‑to‑face training during the COVID-19 lockdown period in 2020 did not have a significant impact on its international operations, because the majority of international students enrolled in courses were in the country when travel restrictions came into effect. The completion of over 60,000 unit enrolments domestically were delayed due to the lack of vocational placements across many industry sectors. Continued border closures are expected to have an impact on new international student intakes as well as migrant and refugee intakes in the 2020–21 financial year.

TAFE Queensland also worked in partnership with the Queensland Government to deliver a range of fully funded and free training options (COVID Safe training modules, online short courses, and skill sets) to support businesses and upskill individuals affected by COVID-19.

Figure 3E shows the financial challenges TAFE Queensland has faced in recent years. However, it also shows that it is projecting an improvement in the 2020–21 financial year. This is largely driven by one-off funding from the Queensland Government to support its operations, without which it will expect another operating loss. Additional initiatives are also being introduced to stimulate training demand and improve future employment opportunities.

Queensland Audit Office.

Significant outlays may be required to achieve longer-term cost savings and efficiencies. TAFE Queensland is continuing with its investment in information technology infrastructure and digital capabilities in the 2020–21 financial year, which it expects will enable operational efficiencies. Without any significant changes in overall market settings, TAFE Queensland will continue to rely heavily in the short to medium term on government grants to cover its operating expenses, particularly employee expenses in order to meet its training commitments and service expectations as a public provider.

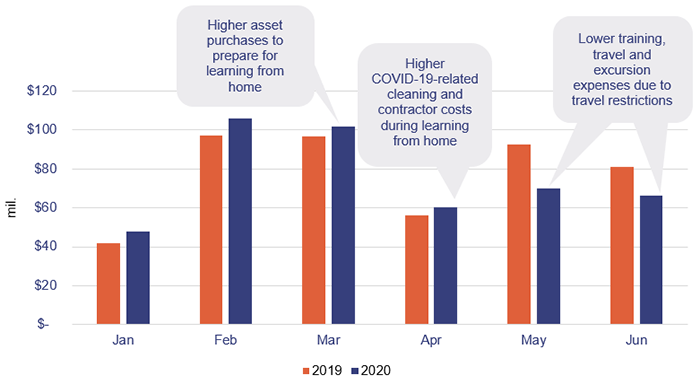

Schools provided home-based learning in 2020

For the first five weeks of term two in 2020, the Department of Education provided remote learning for core content to its students. To ensure students had access to the learning resources they needed, and to support its employees, the department:

- upgraded its information technology operating systems, including security patching, to provide access to improved video and audio tools

- increased information technology infrastructure by adding new servers, increasing the memory and network capacity, and providing new digital learning platforms. In this way, it spread the load of students and staff accessing the infrastructure

- provided 5,550 laptops at a cost of $2.6 million to schools, upon request

- made alternate learning resources available for students with limited or no access to computers and/or the internet.

Queensland Audit Office.

During the learning from home period, schools adopted new technology and digital learning platforms to support new ways of learning, working, and communicating. These will be built into business-as-usual practices. The Department of Education has reviewed the response to the COVID-19 pandemic and is intending to assist schools to develop technology-based approaches to learning.

We plan to issue a report to parliament on how the department is connecting learners and staff of state schools to digital resources and online content.

Asset management at education entities

Universities manage large asset portfolios (worth $9.1 billion at 31 December 2020). As part of their response to COVID-19, the universities took the opportunity to reassess their asset maintenance and investment programs to align these to their strategic goals.

The Department of Education and the Department of Employment, Small Business and Training also manage large asset bases, accounting for $22.8 billion at 30 June 2020. Under an agreement, the Department of Employment, Small Business and Training allows TAFE Queensland to use its buildings for vocational education.

Effectively managing large and widely disbursed asset bases is vital for these entities if they are to continue delivering their services to the broader community. Planning the timing and nature of future investment (construction of new schools or expansion of existing schools) is essential to supporting local communities.

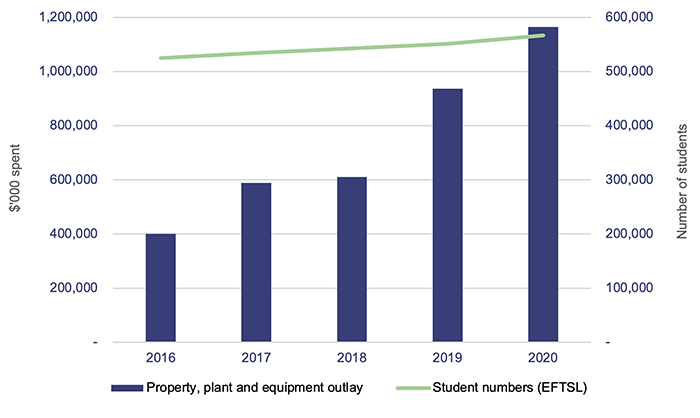

Increased investment in new schools

The Department of Education has heavily invested in its property, plant and equipment assets (mostly schools and buildings) in the last five years ($3.7 billion) to ensure it is prepared for the future and for growing student numbers.

Note: EFTSL—equivalent full-time student load.

Queensland Audit Office.

Since 2016, it has opened 26 new schools within Queensland and will open a further three new schools in 2022. It also has large expansion programs for new and existing schools, to ensure they have the capacity to service their communities. This is a significant outlay for the department, with $1 billion in planned spending over the next four years.

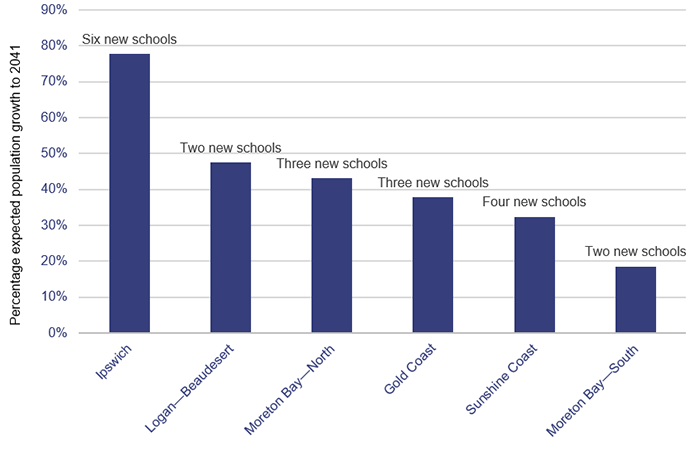

The Queensland Government Statistician’s Office has projected a population growth of 26 per cent for school-aged children from 2021 to 2041. Population growth in this demographic varies across the state, with Ipswich expected to grow 78 per cent, while outback Queensland is expecting a decline of 11 per cent. The department has been constructing new schools in the areas with highest projected population growth, building at least two new schools in the last five years for the top five regions.

Another consideration for the construction of new schools is the class size target guidelines provided by the department. Currently, 97.6 per cent of classes are achieving the targets. The Moreton Bay—South region currently has the lowest rate of compliance, with only 93.2 per cent of its classes achieving the targets. This region has seen significant population growth in the last five years, which has contributed to this result.

Queensland Audit Office.

Figure 3H shows that the department has been focusing on building schools in regions that are expecting significant population growth, or to assist them in meeting their class size target. The three schools being constructed for opening in 2022, as well as the majority of expansions to existing schools, are all in high population growth areas. The department needs to ensure its digital strategy is integrated with its planning for new and existing schools.

Maintenance programs are being updated

Education entities must undertake regular renewal and maintenance activities to ensure existing assets continue to be fit for purpose and to accommodate changing learning styles.

To determine maintenance plans, the Department of Education and the Department of Employment, Small Business and Training each undertake an asset condition assessment. This process takes time, and the last full round of assessments was undertaken between

2016–2018. For maintenance planning purposes, this means some information is up to four years old.

The Department of Education and Department of Employment, Small Business and Training will be undertaking assessments from next year to update information on the current condition of their assets, to use in their forward maintenance programs.

Having well-developed maintenance plans for these assets is critical if the departments are to deliver their strategic goals. Without effective maintenance plans in place, asset renewals may be completed haphazardly, or only in response to the identification of significant defects.

Recommendation for all entitiesImprove asset condition assessments (REC 3) |

|

All entities need to regularly review the condition of their assets to ensure they understand current and future maintenance requirements. Entities need to use accurate information about the condition of their assets to inform their long-term asset management strategies, which should consider both physical assets and digital infrastructure. |

Investment continues in air conditioning and solar panels for schools

The Queensland Government announced in February 2020 that it would be investing $477 million into Queensland schools to ensure that all classrooms, libraries, and staff rooms are air conditioned by the end of July 2022, and to expand the existing Advancing Clean Energy Schools program (which installs solar panels at schools).

Based on the last four comprehensive revaluations undertaken for the Department of Education, 41 per cent of its buildings are currently air conditioned. The department will need to continue to monitor the rollout of this program and the impact it has on its forward maintenance planning.

2020 education dashboard

Our interactive map of Queensland allows you to explore information on education entities and compare to other regions, including data on revenue, expenses, assets, liabilities and other measures like student and staff numbers.