Overview

The entities in Queensland's health sector work together to provide a range of healthcare services to Queenslanders and support the wellbeing of Queensland communities. This year, they were also at the frontline of the battle against COVID-19, which brought a wide range of impacts across the sector.

Tabled 9 February 2021.

Report on a page

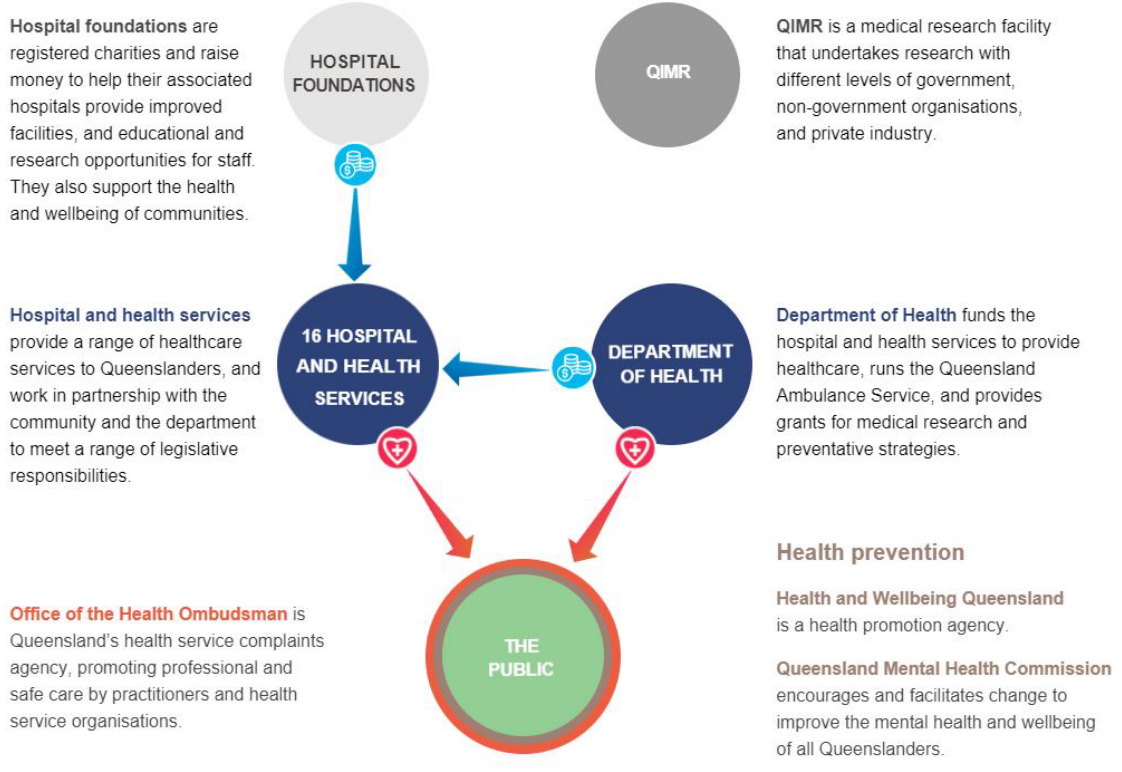

This report discusses the audit results of Queensland health entities, which include the Department of Health (the department) and 16 hospital and health services (HHSs). The report also summarises the audit results for 12 hospital foundations and four other statutory entities.

Financial statements are reliable

The financial reports prepared by Queensland health entities, most hospital foundations, and the four other statutory bodies are reliable and comply with relevant laws and accounting standards.

Some systems and processes have been ineffective

In our recent report to parliament—Queensland Health’s new finance and supply chain management system (Report 4: 2020–21)—we found the department experienced significant issues after implementing its new finance system.

As a result of these issues, the HHSs could place only limited reliance on the finance system’s purchasing controls for their goods and services. We also were unable to rely on these controls in conducting the audit, which led to additional work and cost for the Queensland health entities and us.

The health entities still have some manual recording and reporting processes, which should be automated if possible.

Some health entities have still not addressed internal control deficiencies we identified in previous financial years. These include deficiencies in purchasing processes and controls. Also, after eight years of operations, not all HHSs have approved service level agreements with the department for the purchasing and payroll services the department performs on their behalf.

Impact of COVID-19

The health sector is at the frontline of the battle against COVID-19 and is being successful in containing the spread of the virus. The Queensland Government signed an agreement with the Australian Government to help the public and private health sectors respond to COVID-19.

Queensland Health received $345 million to fund personal protective equipment, fever clinics, community screening, and other costs associated with preparing and responding to the pandemic.

Queensland’s compliance with the Australian Government policy of temporarily suspending all non-urgent elective surgeries temporarily reduced the number of typically high volume, non‑urgent procedures performed at HHSs. COVID-19 has resulted in a decrease in own‑source revenue from private patients and increased employee expenses to respond to the pandemic.

Financial sustainability of HHSs continues to decline

In 2019–20, 11 out of 16 HHSs reported operating losses (three more than last year), despite only one HHS having budgeted for an operating loss in 2019–20. Seven HHSs have now made an overall loss since they were formed in 2012. The former Minister for Health and Ambulance Services appointed advisors to two HHS boards in response to ongoing financial sustainability issues.

Recommendations for entities

Automate manual financial reporting processes (Queensland health entities) |

|

|

Queensland health entities should improve the efficiency of their reporting by automating manual processes, where possible. |

|

Resolve outstanding audit issues (Queensland health entities) |

|

|

Queensland health entities and their audit committees should continue to regularly review the status of outstanding audit issues and ensure they are resolved in a timely manner. |

|

Strengthen the security of information systems (all entities) |

|

| REC 3 |

We recommend all entities strengthen the security of their information systems. They rely heavily on technology, and increasingly, they have to be prepared for cyber attacks. Any unauthorised access could result in fraud or error, and significant reputational damage. Their workplace culture, through their people and processes, must emphasise strong security practices to provide a foundation for the security of information systems. Entities should:

Entities should also self-assess against all of the recommendations in Managing cyber security risks (Report 3: 2019–20) to ensure their systems are appropriately secured. |

Approve service agreements for shared services (Queensland health entities) |

|

| REC 4 | The Department of Health and the hospital and health services should work together to approve and sign service level agreements with each other for the purchasing and payroll services the department performs on behalf of the HHSs. The agreements should clearly identify the roles and responsibilities of each party, including the quality and scope of services and the respective costs. |

Address backlog of asset maintenance (Queensland health entities) |

|

| REC 5 |

Queensland health entities should continue to prioritise high-risk maintenance. The hospital and health services should work with the department to find ways to mitigate the operational, clinical, and financial risks associated with anticipated maintenance. |

1. Overview of entities in this sector

Queensland Audit Office.

2. Results of our audits

This chapter provides an overview of our audit opinions for the entities in the health sector. It also provides conclusions on the effectiveness of the systems and processes (internal controls) entities use to prepare financial statements.

Chapter snapshot

Financial statements are reliable

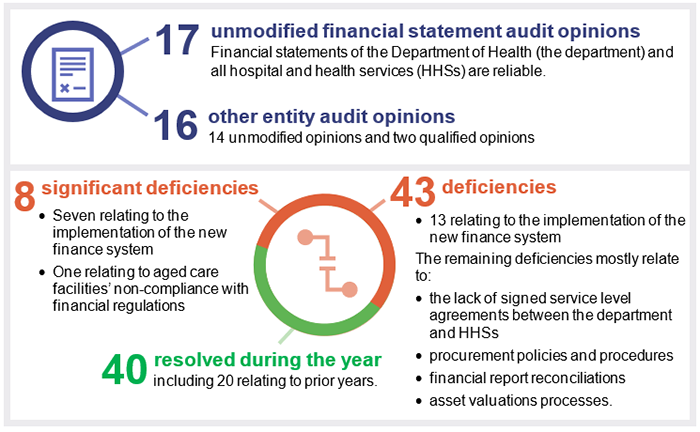

We issued unmodified audit opinions to all 17 Queensland health entities (the department and the 16 HHSs). Readers can rely on their audited financial statements. All Queensland health entities finalised their financial reports within their legislative deadlines. This is a good achievement given the impact of COVID-19 on staff and the issues with the implementation of the new finance system.

None of the annual reports were tabled by the legislative date of 30 September 2020. The HHSs’ annual reports were tabled in parliament on 14 December 2020, and the department’s annual report was tabled on 15 December 2020. This is the second time in three years all the Queensland health entities’ annual reports have not been published by their due date. Unless the appropriate minister extends the time frame, Queensland legislation requires departments and statutory bodies to table their annual reports in parliament within three months after the end of the financial year.

We also audited 12 hospital foundations and four other statutory bodies. All 16 entities, except for Townsville Hospital Foundation and Gold Coast Hospital Foundation, received an unmodified opinion. The qualified opinions for these two entities were due to the lack of appropriate controls to ensure all cash donations from the public and revenues from sales of goods were recorded. Bundaberg Hospital Foundation and Townsville Hospital Foundation did not finalise their financial reports within the legislative deadline.

Appendix D details the audit opinions we issued.

We express an unmodified opinion when the financial statements are prepared in accordance with the relevant legislative requirements and Australian accounting standards.

We express a modified opinion when financial statements do not comply with the relevant legislative requirements and Australian accounting standards and, as a result, are not accurate and reliable.

A modified opinion can qualify only certain aspects of the financial statements that are not prepared in accordance with the relevant legislative requirements and Australian accounting standards.

Not all entities in the health sector produce financial statements. Appendix F lists the entities not preparing financial statements and the reasons.

Other audit and assurance opinions

Appendix E lists the other audit and assurance opinions we issued.

For the fourth time in five years, we issued a qualified audit opinion for the annual ‘prudential compliance statement’ for Queensland Health’s aged care facilities across four HHSs.

In this statement, Queensland Health is required to outline to the Australian Government how it has managed refundable accommodation deposits, accommodation bonds, and entry contributions from aged care residents. We qualified our audit opinion because of significant non-compliance with several financial regulations. For example, the aged care facilities did not provide evidence that they have completed accommodation agreements with residents within the legislative time frame.

Queensland health entities assessed their financial statement preparation processes as mature

We worked with the department and the HHSs as they undertook a self-assessment of their financial statement preparation processes using the maturity model on our website.

In general, the entities assessed themselves as having mature financial statement preparation processes. They rated many elements of their financial statement preparation processes as either ‘integrated’ or ‘optimised’ (the two highest levels of maturity). This means they have assessed their processes for supporting the preparation of financial statements as efficient and as providing high‑quality information in a regular, timely manner.

Figure 2A outlines the entities’ self-assessed strengths and opportunities.

| Strengths |

|

| Opportunities for improvement |

Common opportunities for Queensland health entities included:

Common opportunities for some HHSs include:

|

Queensland Audit Office.

Recommendation for Queensland health entitiesOpportunities to automate manual financial reporting processes (REC 1) |

| Queensland health entities should improve the efficiency of their reporting by automating manual processes, where possible. |

Not all systems and processes for purchasing goods and services were effective

We assess whether the internal controls entities use to prepare financial statements are effective. If we find issues in internal controls, we identify them as either significant deficiencies, that require immediate action by management, or deficiencies, that management can correct over time.

We found Queensland health entities’ internal controls within the new finance system were not effective. As a result, we were not able to rely on them for our audits, which meant additional work and cost.

Figure 2B shows the number of internal control deficiencies we have raised in each of the last three financial years, and their status at 31 August 2020. Of the 51 new issues we have identified in 2019–20, 20 relate to the implementation of the new finance system.

Note: One deficiency, relating to the lack of a signed service level agreement between the department and a HHS, remains outstanding from 2014–15.

Compiled by Queensland Audit Office.

Issues identified in previous years

Of the deficiencies raised between 2014 and 2019, 27 per cent remain unresolved. These mostly relate to procurement processes and controls, and to HHSs not having signed service level agreements with the department for the operational services they use. By not resolving audit issues in a timely manner, entities are unnecessarily exposed to risks that should have been mitigated. All entities should proactively work to resolve outstanding issues by their implementation date.

Recommendation for Queensland health entitiesResolve outstanding audit issues (REC 2) |

| Queensland health entities and their audit committees should continue to regularly review the status of outstanding audit issues and ensure they are resolved in a timely manner. |

We identified significant deficiencies with the implementation of the new finance system

On 1 August 2019, the department launched its new finance system. In our recent report to parliament—Queensland Health’s new finance and supply chain management system (Report 4: 2020–21)—we found the department experienced significant issues after implementing the finance system. The department identified little to no adverse impact on patient care.

The department did not clearly document its internal controls prior to the system going live

The department provides critical purchasing, payroll, and information technology services to the HHSs. This includes designing and operating the relevant purchasing and payroll controls that directly impact on their ability to prepare true and fair financial statements. The controls also impact on the accuracy of management reports that rely on information from the finance system.

From when the system went live on 1 August 2019 until 24 November 2019, we were unable to audit the department’s information technology and purchasing controls. This was because the department had not documented descriptions of the internal controls prior to the system going live, and it was amending controls and stabilising the system.

Without independent assurance on the effectiveness of the system's internal controls, HHSs faced a greater risk of fraud or error when processing transactions in the system.

The department’s new finance system controls did not operate effectively

We identified six significant control deficiencies relating to the implementation of the finance system. These issues primarily related to user access to the system and to information security, including:

- inappropriate configuration of the system, which did not protect financial data from deletion

- inappropriate allocation and maintenance of user access to the system

- inappropriate validation of bank account information in the system.

As a result, the department and the HHSs could only place limited reliance on the finance system controls that prevent or detect errors in expenditure transactions. We did not find evidence that anyone intentionally exploited these weaknesses.

Consistent with the experience of Queensland health entities, management of user access is a common issue identified across the public sector. Other common weaknesses relate to the ongoing maintenance of systems, which Queensland health entities will need to establish appropriate processes for in the future. We have made the following recommendation for all entities across the public sector. This is to highlight the importance of protecting information systems so entities are not exposed to loss of sensitive information or valuable assets.

Recommendation for all entitiesStrengthen the security of information systems (REC 3) |

|

We recommend all entities strengthen the security of their information systems. They rely heavily on technology, and increasingly, they have to be prepared for cyber attacks. Any unauthorised access could result in fraud or error, and significant reputational damage. Their workplace culture, through their people and processes, must emphasise strong security practices to provide a foundation for the security of information systems. Entities should:

|

The department and HHSs do not have approved service level agreements

We continue to raise control deficiencies with the department and the HHSs because they do not all have signed service level agreements that outline the cost and scope of services the department provides to the HHSs.

Only two HHSs have signed their service level agreements for operational support services such as the provision of linen and of pathology. Only five HHSs have signed their service level agreements for information and communication technology support with the department.

Without signed service agreements, there is a lack of accountability and an increased risk of gaps and weaknesses in the services the department provides to the HHSs. This may lead to fraud or errors when processing transactions.

Recommendation for Queensland health entitiesApprove service agreements for shared services (REC 4) |

|

The department and HHSs should work together to approve and sign service level agreements with each other for purchasing and payroll services the department performs on behalf of the HHSs. The agreements should clearly identify the roles and responsibilities of each party, including the quality and scope of services and the respective costs. |

3. Impact of COVID-19

The health sector is at the frontline of the battle against COVID-19. Our report to parliament—Queensland Government response to COVID-19 (Report 3: 2020–21)—provided an overview of the measures announced by the Queensland Government up to 21 August 2020.

Chapter snapshot

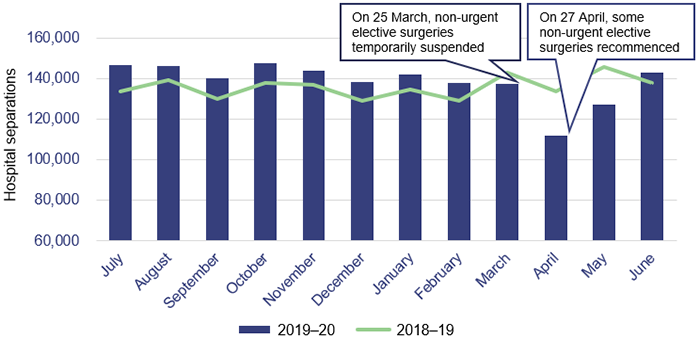

The number of hospital separations and surgeries decreased because of COVID-19

Separations are the total number of episodes of care for admitted patients, which include total hospital stays (from admission to discharge, transfer, death or change of type of care).

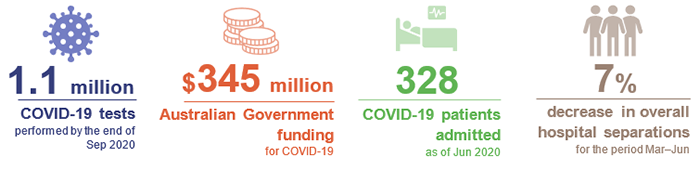

As shown in Figure 3A, from March to June 2020, there was a decrease in hospital separations because of COVID-19. Hospital and health services (HHSs) admitted seven per cent less patients than in the same period the previous year.

Queensland Audit Office from the HHSs' hospital separations data.

The Australian Government’s policy to temporarily suspend all non-urgent elective surgeries reduced the number of typically high volume, non-urgent procedures in Queensland hospitals. Comparing March to June 2019–20 to the same period in 2018–19, the most significant reductions were in the following specialty areas:

- ear, nose, and throat—down 33.5 per cent. Non-urgent procedures include removing tonsils

- ophthalmology—down 34.8 per cent. Non-urgent procedures include cataract surgery

- orthopaedics—down 35.3 per cent. Non-urgent procedures include knee surgery and associated procedures.

Physical distancing practices to prevent community transmission of COVID-19 also significantly helped to reduce the severity of Queensland’s flu season in 2020. Between January and October 2020, Queensland Health recorded 6,008 cases of the flu, which is 60,000 less than the same period in 2019. This contributed to a 22 per cent reduction in hospital admissions relating to respiratory medicine.

Ordinarily, delivering less patient activity would result in less revenue for hospitals, which are funded on the basis of the activities they carry out. However, in response to COVID-19, the Queensland and Australian governments guaranteed state and HHSs’ funding based on the 2019–20 patient activity targets. This arrangement is continuing in 2020–21. Some HHSs experienced a decrease in own-source revenue from private patients.

National funding agreement to reimburse COVID-19 costs

The Queensland Government has signed a National Partnership Agreement with the Australian Government. The agreement provides funding to support the health sector’s response to COVID‑19, including for:

- diagnosing and treating COVID-19 cases in private and public hospitals

- specific costs incurred in preparing and responding to COVID-19 in public hospitals

- providing additional emergency staffing and accommodation in aged care facilities

- ensuring private hospitals remain financially viable over the COVID-19 pandemic, in return for agreeing to provide their facilities, staff and supplies to support the COVID-19 response. Twenty-eight private hospital operators signed the agreement with the Queensland Department of Health.

The agreement includes funding for personal protective equipment, fever clinics, community screening, and other costs associated with preparing for and responding to the pandemic. The National Partnership Agreement does not compensate HHSs for indirect COVID-19 impacts, such as increased employee expenses and reduced own-source revenue from private patients.

In 2019–20, Queensland health entities received up to $345 million under the agreement, consisting of:

- $207 million in Australian Government funding relating to payments to ensure private hospitals can operate viably and to support the COVID-19 response

- $118 million relating to state public health and hospital payments, which was funded equally by the Queensland and Australian governments

- $20 million in Australian Government funding for up-front advance payments.

Employees are taking less leave due to COVID-19

HHS employees took less annual leave in the final five months of 2019–20 compared to the same period in 2018–19. In 13 of the 16 HHSs, employee annual leave expenditure was more than 10 per cent lower in 2019–20 than in 2018–19. In the short term, this will increase costs because the HHSs paid salaries and wages for a greater portion of 2019–20, while employees also earned leave entitlements.

It also presents an operational and financial challenge to HHSs in the medium term. As employees take higher rates of leave in the future, HHSs will need to ensure they have appropriate capacity to maintain health services. This could lead to additional spending on temporary labour or employee overtime.

4. Ongoing decline in financial sustainability

Chapter snapshot

Compiled by Queensland Audit Office from the HHSs’ financial statements.

HHSs’ operating losses increased

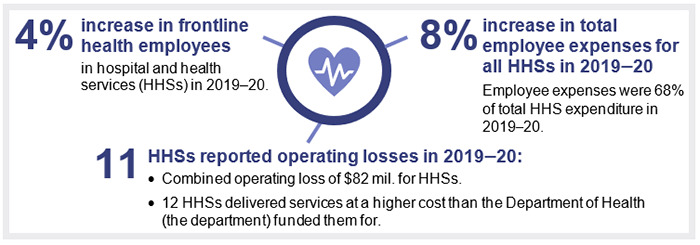

The HHSs’ combined operating loss in 2019–20 was $82 million (2018–19: $34 million). Eleven of the 16 HHSs reported an operating loss—three more than last year.

Seven out of 16 HHSs have now accumulated an overall loss since they formed in 2012, which is three more than in 2018–19 (Appendix G lists these HHSs). The former Minister for Health and Minister for Ambulance Services appointed board advisors to help Sunshine Coast and North West HHSs deliver operational efficiencies in response to their financial results.

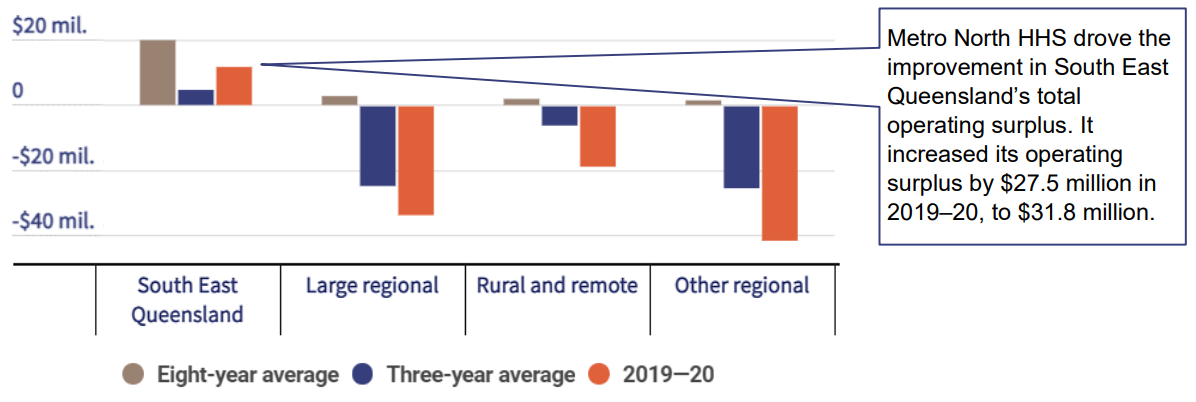

Figure 4A shows each HHS region’s operating result for 2019–20 compared to its three-year and eight-year averages.

Note: Appendix B shows how the HHSs are grouped into regions. See Appendix G for individual HHS financial results.

Queensland Audit Office from HHSs’ financial statements.

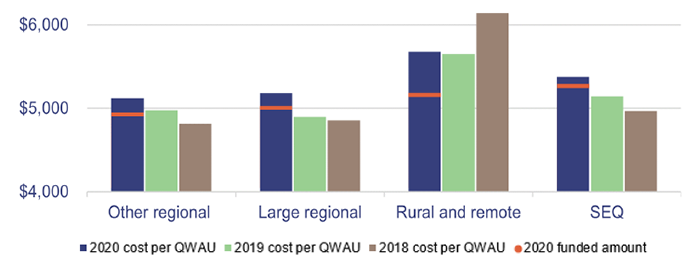

The department funded most of the HHSs based on the number and complexity of clinical services provided to patients. To measure this, the department standardises health activity into Queensland weighted activity units (QWAU). For example, a HHS would record a higher number of QWAUs for delivering complex surgery than for a simple day procedure.

The HHSs’ operating losses are increasing because, while they were funded for $5,033 per QWAU in 2019–20, the cost of delivering a QWAU in 2019–20 was, on average, $5,161.

Increasing employee expenses over the year for salary increases, overtime, allowances and additional staff are mostly responsible for the increasing cost per QWAU in HHSs. In 2019–20, employee expenses increased eight per cent to $778 million, and are now 68 per cent of total HHS expenses. While not all of this increase was a direct result of COVID-19, it did contribute to HHSs' increasing net costs and declining financial results.

As Figure 4B shows, HHSs in all regions have not been able to deliver sufficient savings to close the gap between the cost and funding to deliver a QWAU. The cost to deliver QWAUs has increased in all regions over the last three years, except at North West HHS within the rural and remote region.

Queensland Audit Office.

The department has applied efficiency and productivity dividends on HHSs. Efficiency dividends encourage HHSs to identify cost savings by reducing how much the department funds HHSs without reducing their target level of QWAUs. With productivity dividends, the department increases the HHSs' expected activity output without a corresponding increase in the funding they provide.

The department is also implementing a new way of measuring the labour that HHSs require to deliver health services. Previously, the department’s analysis and reporting on HHSs' labour excluded some elements of the workforce such as contractors, consultants and the amount of overtime HHSs incur. It now includes those elements, which provides a more holistic view of the workforce.

Aiming to control labour costs, the department is using its new measure of labour to set sustainable labour targets for each HHS. These targets will be difficult for some HHSs to achieve while maintaining performance targets.

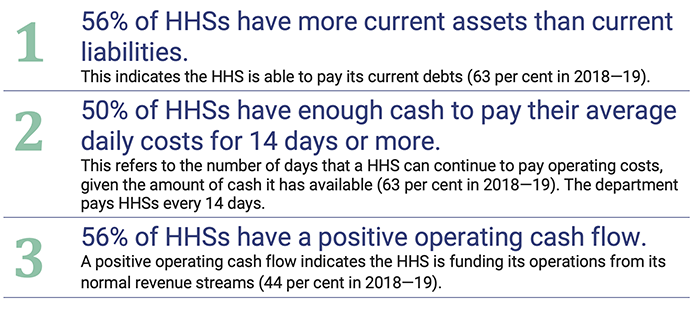

HHSs have less cash available to pay their bills

Five of 16 HHSs failed to meet all three of our better practice financial benchmarks (see Figure 4C) in 2019–20 (refer to Appendix H for a more detailed explanation of our financial benchmarks). These provide insights into the financial sustainability of the HHSs. Four of the five are from the rural and remote or other regional HHS groups.

These HHSs may not have enough cash to pay for significant expenditure items as they arise, for example, construction payments. This means they may choose to hand back the operational management of these projects to the department.

Note: ‘Current’—for assets, liabilities, and debts—means they will be available, used, incurred, or need to be paid in the current financial year.

Queensland Audit Office from HHSs' financial reports.

The department is helping HHSs access more cash

The department is using the following two methods to ensure HHSs have access to enough cash to pay their bills, when needed.

| Method | Detail |

|---|---|

| Cash advances |

HHSs can request advance cash payments of their fortnightly funding from the department. In 2019–20, the department paid $8.92 million in cash advances to three HHSs. In all cases, the department recouped the cash advance by reducing future fortnightly payments. |

| Increasing overdraft facility |

The HHSs’ total overdraft facility with Queensland Treasury increased from $100 million to $200 million. An overdraft facility enables HHSs to access cash to pay suppliers and continue operations in the event of temporary cash shortfalls. As at 30 June 2020, only North West HHS had drawn on its overdraft facility (by up to $3.35 million, out of a total limit of $4 million). |

Queensland Audit Office from HHSs' financial reports.

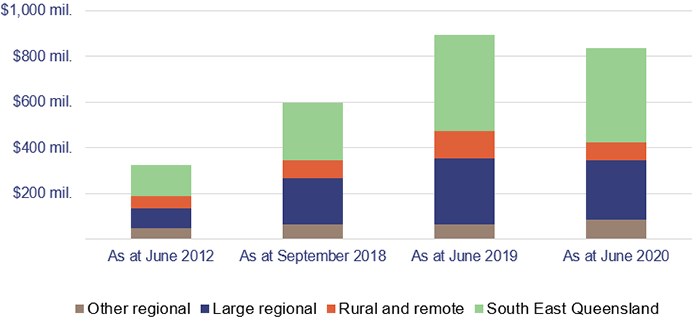

HHSs face challenges in funding building maintenance

HHSs face a significant future challenge in funding the anticipated maintenance of their buildings. To comply with the Queensland Government’s maintenance management framework, all Queensland health entities report on their anticipated maintenance (often referred to as deferred maintenance in other sectors). HHSs’ anticipated maintenance has increased significantly since 2012, and they will need to dedicate increasing proportions of their future budgets to this.

Figure 4E details the anticipated maintenance costs for HHSs by region. Across the HHSs, the value of anticipated maintenance decreased by $57 million in 2019–20, while HHSs' total repairs and maintenance expenses increased by less than $2 million.

Note: The June 2012 column relates to immediately before HHSs were formed on 1 July 2012.

Queensland Audit Office from the HHSs’ annual reports.

Recommendation for Queensland health entitiesAddress backlog of asset maintenance (REC 5) |

|

Queensland health entities should continue to prioritise high-risk maintenance. The hospital and health services should work with the department to find ways to mitigate the operational, clinical, and financial risks associated with anticipated maintenance. |

2020 hospital and health service dashboard

Find your local hospital and health service (HHS) in this Queensland Audit Office visualisation to explore its financial audit data for 2020 and compare to other hospital and health services. This interactive tool includes data on revenue, expenses, assets, liabilities and activity measures.