Overview

Councils are responsible for the long-term upkeep of local roads, water and sewerage, town and land planning, building approvals, and animal control for their communities. As Queensland councils own and operate approximately $114 billion worth of infrastructure assets, it is pivotal they manage them effectively. This means council leaders require accurate information on the status, condition, and value of their assets so they know how much revenue they need to maintain them and so they can make informed investment decisions.

Tabled 25 July 2023.

Auditor-General’s foreword

Queensland's 77 councils provide vital infrastructure services that help grow local economies. They deliver roads, water, and sewerage to an estimated 5.3 million people. Some also provide their communities with public open space, public amenities, and cultural facilities such as museums and libraries. A small number operate childcare centres and other businesses. Many people depend on the long-term sustainability of our councils.

A council’s sustainability is more than just financial. It is linked to the success of its local community, where local businesses are economically viable, and people have access to basic services, such as education, employment, housing, and clean water. Communities thrive when councils can afford to operate, maintain, and renew their assets to deliver the level of service the community expects.

This audit on improving asset management in local government is the fourth we have undertaken on the sustainability of the local government sector. The earlier audits were:

- Managing the sustainability of local government services (Report 2: 2019–20)

- Managing local government rates and charges (Report 17: 2017–18)

- Forecasting long-term sustainability of local government (Report 2: 2016–17).

In my previous reports, I made a series of recommendations to councils to improve their management of risks to their sustainability. I also recommended that the Department of State Development, Infrastructure, Local Government and Planning strengthen the analysis and reporting of key sustainability metrics by councils. Appendix E provides a list of the recommendations made in the first 3 audits and other recent reports on the results of local government annual audits.

The department has a role in providing advice to councils on how to manage their assets and in ensuring they comply with the requirements of the Act and regulations. Advice and support can help councils to provide communities with fit-for-purpose and value-for-money services for the long term.

As part of this audit, we surveyed councils on the maturity of their approaches to asset management compared to international better practice. We intend to build on this survey later this year, to develop a maturity model for asset management across all government sectors.

In 2024–25, I will examine the sector’s overall progress in meeting its sustainability challenges. The audit will consider how effectively the sector has acted to address our previous findings and recommendations to councils and the Department of State Development, Infrastructure, Local Government and Planning.

My commitment to the issues affecting the sustainability of local governments and Queensland communities is long standing and well-known. Throughout my term as Auditor-General I have travelled to 66 local governments, including all 17 First Nations councils, to hear firsthand the challenges local governments face. I trust that our focus on sustainability will ensure that council assets are well managed and supported so that councils can afford to deliver the services needed for future generations of Queenslanders.

Brendan Worrall

Auditor-General

Report on a page

Council assets are often expensive and need to last a long time. Asset management plans ensure councils know how much it will cost to maintain and replace their assets as they age. This lets them know how much revenue they need from rates and fees, including the servicing of any borrowings.

Collectively, Queensland councils own and operate approximately $114 billion worth of infrastructure assets. Accurate information on where the assets are, and on their condition and value, helps councils make informed decisions on asset replacement projects, knowing they can afford them for the long term.

This report looks in detail at 5 councils across the state and their approaches to managing their assets. We also surveyed all councils and asked them to self-assess their asset management approaches. We have made recommendations to the 5 individual councils, the whole sector, and the Department of State Development, Infrastructure, Local Government and Planning.

We observed from the self-assessment asset management survey that only 9.6 per cent of councils had an overall maturity average at or above the minimum requirements of the internationally recognised standard for asset management. It highlights the need for stronger leadership to embed asset management processes, including withstanding staff changes and helping councillors to deliver better community services.

Gaps in asset management practices

All 5 councils had developed asset management plans for most of their assets and were using asset information to inform investment decisions for asset projects. However, they could improve the quality of the information to make their decisions by:

- governance – putting in place formal governance groups to ensure asset, finance, and service managers consider and challenge asset plans and projects before going to council for approval

- asset information – regularly assessing if the asset information has changed because of revaluations, natural disasters, changes in condition, or obsolescence, to keep asset plans up to date

- reporting – developing measures and reporting on them so that councils are accountable for how assets contribute to the corporate priorities for the community.

Greater support needed to build asset management capability

The Department of State Development, Infrastructure, Local Government and Planning’s sustainability framework shows how local governments can integrate asset planning and reporting with services and budgets. It also requires councils to report on key sustainability measures, including 3 that focus on asset sustainability. It has not produced detailed guidance for how to develop a long-term asset plan or individual asset plans for each asset class. There are no better practice guidelines or minimum requirements showing councils what to cover in their asset plans.

The department has a role in supporting local governments to be sustainable and in monitoring compliance with the Local Government Act 2009. It has not documented how it will fulfil this role or how it will identify those councils that need help to address risks to the sustainability of their assets and services.

The department offers training workshops to support asset management capability. In the last 3 years, only 21 per cent of councils participated in the training workshops. The department needs to assess what asset management training council leaders and staff need, so it can work with its partners to tailor its programs to those in most need.

1. Audit conclusions

The 5 councils we audited have developed asset management plans as required by the Local Government Act 2009 and the Local Government Regulation 2012. However, they need more guidance to move beyond compliance. They also need to manage their assets effectively to deliver services to their communities, while understanding the full cost of owning the assets. The results of our self-assessment survey show that, on average, councils have significant work to move beyond the ‘basic’ level of maturity to meet the minimum requirements of the international better practice standard.

Managing a diverse portfolio of assets is a complex activity involving multiple areas of a council. Asset managers, the finance team, and service managers need to work together to ensure the council has the assets it needs to support cost-effective service delivery. Councils, to varying degrees, need to do more to manage their assets effectively. The department has an important role to play in this.

Information in asset plans is not current or linked to delivering services

Once councils have developed their asset management plans, they are not following better practice and regularly updating the information in them. If councillors and executive leaders are not confident in the asset information, they could delay decisions to renew or replace ageing assets. It could also result in projects being mis-prioritised, leading to poor investment decisions. Infrastructure assets, by their nature, last a long time, and it can take months of planning to get the designs and budgets developed and approved. Being confident in the data helps councils to make timely decisions to start renewal and upgrade projects before assets deteriorate. This ensures their assets can deliver services that are safe and at the level the community expects, in a way that is equitable and responsible.

Good governance ensures councillors make decisions based on complete and accurate information. Councils can identify gaps or risks if they give relevant areas across each council the opportunity to consider and challenge asset plans. We found inconsistent governance approaches to decision-making for asset renewal and replacement. Without opportunities for their finance, asset, and service managers to have input, councillors may be unaware of the full impacts of their decisions on a council’s portfolio of assets and range of services.

There are opportunities for councils to integrate their asset management plans with their other planning documents. The councils do not have clear links to the services they provide to their communities. Ensuring the asset portfolio supports its goals allows councils to dispose of old assets that are no longer delivering the services people want. Councils can then invest in keeping high-value or critical assets in good condition, delivering more efficient (greater productivity at a lower cost) services, or acquiring new assets to deliver new services.

The councils do not report to their communities on the performance of their assets in delivering effective or efficient services. They set service targets but do not monitor whether they were achieving them or at what cost. Without information on how well the assets are delivering services based on the current investment, they cannot assess if they need to invest more or less. The asset management plans do not show that they can afford to achieve their service targets for the long term or if the assets are providing the value envisaged in the investment decision.

Self-assessed gaps in levels of asset management maturity

We asked councils to self-assess the level of maturity of their approaches to asset management. This was a self-assessment; we provide no assurance that the ratings reflect the actual maturity of councils' approaches. However, the results do provide the department with critical information on councils’ views of the gaps in their current level of maturity.

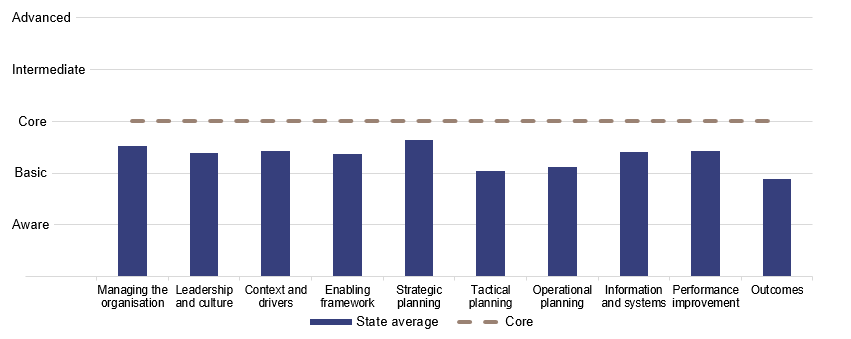

The survey results show that, on average, councils still have some way to go to meet the minimum (core) requirements of the international better practice standard. They need much more guidance and significant support from the department to make the progress required. Figure 1A shows how the state average compares to the core rating (3) of the international standard for asset management systems. To meet the minimum requirement of the standard, councils had to score 3 or more on our survey.

Note: We have not audited these self-assessments.

Queensland Audit Office, Asset management maturity survey.

The 5 levels of maturity based on the requirements of the international standard:

Advanced Processes are optimised with no improvements needed

Intermediate Has sound processes; however, improvements could be made

Core Meets the minimum requirements

Basic Partially meets requirements

Aware Does not meet the legislative requirements

The department can do more to support councils to develop asset planning capability

The Department of State Development, Infrastructure, Local Government and Planning is rolling out a framework to support council sustainability (including a focus on asset management). It requires councils to develop key asset plans and report on key sustainability ratios. But the department needs to provide more guidance for councils on how to develop key asset management documents in line with better practice.

Councils need more support so they can develop robust asset planning documents aligned with their services and budgets. This will allow them to be confident they can afford to operate, maintain, and eventually replace their assets over the long term.

Council reports on sustainability ratios can provide the department with historical trends, but the reports may not give it sufficient information to identify which councils need help. The department does not fully detail how it will support councils that persistently do not meet the targets of the asset sustainability ratios.

In 2022, in our report Improving grants management (Report 2: 2022–23) we recommended departments assess the risk that decisions to award grants are based on incomplete or inaccurate information. Requiring councils to include current asset management plans as part of grant applications for significant infrastructure would reinforce to councils the important role of these documents. It would give the department an understanding of how the proposed project fits within councils’ long-term plans. Critically, it could show the department that the costs of operating and maintaining new assets will not affect councils’ ongoing sustainability.

The department is coordinating with its partners to train council staff to become confident and competent in managing assets. However, council participation at the workshops and webinars is low. The department needs better information on the capability gaps of those with a role in asset management to ensure its training programs are targeting those skills. It may also need to consider if it can provide more incentives to increase participation and build capacity with the range of available providers.

The department provides training to new councillors on financial management issues, but not specifically on their roles and responsibilities for asset management. Tailored training is needed at all levels, including councillors and executives, on why asset management is important. Understanding how to interpret the results of the asset plans is critical to ensuring that decisions are based on well-informed analysis and processes.

2. Recommendations

We have developed the following recommendations for all councils and for the Department of State Development, Infrastructure, Local Government and Planning.

|

Chapter 3 – Gaps in asset management |

|

We recommend all councils assess whether their:

We recommend all councils:

|

|

Chapter 4 – Greater support is needed to build asset management capability |

|

We recommend the Department of State Development, Infrastructure, Local Government and Planning:

|

Reference to comments

In accordance with s. 64 of the Auditor-General Act 2009, we provided a copy of this report to relevant entities. In reaching our conclusions, we considered their views and represented them to the extent we deemed relevant and warranted. Any formal responses from the entities are at Appendix A.

3. Gaps in asset management

Queensland councils are responsible, under the Local Government Act 2009 or the City of Brisbane Act 2010 (the Acts), for ensuring the accountable, effective, efficient, and sustainable management of assets, infrastructure, and services (for example, local roads, water and sewerage, town and land planning, building approvals, and animal control). Councils rely heavily on assets to deliver these services. In 2022, the value of council infrastructure assets (such as roads, bridges, water, wastewater, fleet, and buildings) was approximately $114 billion.

This chapter reports on the gaps in how the 5 councils have managed assets. It also reports on the opportunities for councils to integrate their asset management plans with their service planning.

We selected 5 different sized councils across the state to get a broad understanding of their practices and challenges. The results at the 5 councils cannot be used to extrapolate the results across all councils. However, all councils can consider the recommendations to determine if they are relevant and if the council could improve its asset management approaches to become more sustainable while delivering better services for communities.

A sustainable council can afford to undertake regular maintenance of its assets, which means it can keep them to a standard that allows them to function as designed, and not deteriorate. For example, a sustainable childcare service collects sufficient fees from parents/guardians to cover (if operating on a break-even basis) all its operating costs such as electricity, wages, and consumables (such as paint, paper, and toys). Fees also cover asset maintenance costs, so the council can fix blocked drains or leaking roofs that may shorten the building’s life.

Sustainable services: If a service is sustainable, it means a council can continue to provide it in the long term (10 years). It also means the council can meet the expected service level within its existing budget.

Services range from safe roads and drinking water to accessible libraries, art galleries, and tourist information. Council services all rely on having functioning assets in good condition.

Service levels: A description of the quality of the service council provides. This is different for different types of assets. The levels can relate to the physical condition (smooth roads), quantity/access (available 5 days or 7 days a week), aesthetics (buildings look good, fresh paint and new carpets) or responsiveness (leaks fixed in 24 or 48 hours). They can be customer focused (is the road bumpy?) or technical (inspections completed weekly).

The level can have a significant impact on the cost and therefore sustainability of a service. Councils need to balance the level of the service with the impact on the budget. For example, the service level:

- for a park its often set by the frequency of maintenance work, such as mowing. The more frequently mowing and weeding occurs the more staff (wages) and equipment (assets) are needed. The service level impacts the budget as wages, maintenance of the equipment, and operating costs (fuel) are a major cost of achieving the level of service.

- for roads it often includes how long it takes to repair potholes – a target of 24 hours compared to one week. The service level impacts the budget as council needs extra staff (wages) and equipment (assets) to have the capacity to respond more quickly.

As part of the audit, we asked a broader group of councils (52 of 77 councils responded) about the maturity of their approaches to asset management and the challenges they faced. We have included these observations in the report as context, but they did not inform our conclusions about the 5 councils we looked at in detail. The responses from the broader survey were based on self-assessments and were not audited. Appendix C includes a summary of the councils’ assessments of how well they manage their assets.

We also continue to report issues with council asset management across the whole sector (not just the 5 in scope for this audit). In our report Local government 2022 (Report 15: 2022–23) we raised several asset management issues, including:

- of the 77 councils, 54 have at least one internal control deficiency in their asset management practices

- 17 councils had to correct prior year asset amounts in this year’s financial statements because they found significant prior period errors – a combined total of $241 million

- 12 councils identified assets worth $180 million that they owned but had not previously recorded in their asset registers.

Summary of the key gaps in asset management across the 5 councils

We identified a range of gaps in the approaches to asset management at the 5 councils. We raised individual issues and recommendations to each council. Figure 3A summarises the gaps across the areas audited: governance, systems, and capability.

| Areas audited | Number of the 5 councils with gaps in asset management |

| Governance | |

|

Asset governance groups not in place to have input into key decisions |

3 |

|

Asset management plans not in place for all assets |

3 |

|

Asset data in management plans not current |

5 |

|

Asset management plans not aligned with services and budgets |

4 |

|

Systems |

|

|

Asset systems not integrated |

4 |

|

Council not reporting on the performance of assets |

5 |

|

Capability |

|

|

Asset management training not planned and coordinated |

5 |

Queensland Audit Office.

Better governance is needed for asset management

We found that 3 of the 5 councils did not have formal governance in place to ensure that the right people and areas within council are consulted on asset management decisions. Without input and oversight from formal governance groups, councils may not consider the impact on council services, budgets, and the portfolio of all their assets when making decisions on:

- starting new asset projects

- upgrades to assets

- major and annual maintenance programs.

There is a risk that a council could make decisions about assets without fully understanding the effects on its ability to be able to afford to deliver its services for the long term. For example, a council could underestimate the cost of relocating a library and installing new underground network cables if it does not consider the effects of upcoming road resurfacing or nearby underground infrastructure.

The 2 councils that had formal governance committees in place had oversight of strategic asset management planning, budgets, and service impacts. Their terms of reference covered:

- the purpose, responsibilities, and powers of the committee, including helping to implement good practice in asset management and being a forum for improvement and changes

- membership across council, which included representatives from the asset, finance, and service manager teams

- responsibility for ensuring asset actions and decisions are in line with the council’s corporate goals, strategies, and delegations.

Although another council had developed terms of reference for a committee, we found the committee had yet to meet and oversight was not occurring.

|

Maturity self-assessment Self-assessment of ‘enabling framework’ from our survey The state average for this element is 2.4 which is at the basic level. The basic maturity level means that:

Note: we have not audited these self-assessments. |

Good governance rests on having reliable information about how existing assets are performing and if they are wearing out earlier or later than expected. Case study 1 (Figure 3B) is an example of a council that did not have this information. Figure 3B shows how the council did not update the information in its asset management plan with current information. As a result, it was not able to plan ahead and budget to replace a sewage plant.

| Maintaining an asset with a long life |

|

Background This council owns a 20-year-old sewage treatment plant providing services to approximately 330 people.

Impact The council was not receiving regular reports on the level of service from this asset, including if it was compliant with environmental regulations. It did not challenge the results of the 2021 inspection, despite complaints from the community. The information in the asset management plan was not up to date. Council was not maintaining the asset appropriately, and it had deteriorated significantly earlier than expected. This meant council was not able to budget to maintain the expected level of service (in terms of environmental conditions) and protect the town’s water supply. If the grant application had not been successful, the level of service would have deteriorated, with further impacts on the environment and potential health issues for the community. |

Queensland Audit Office, from council documents.

Leadership and culture is one of 10 the key elements (see Appendix C) of asset management. Critical to achieving lasting and positive change in any organisation is culture, which is set by leaders at all levels. The tone set by leaders is a precondition for success. They set the culture by modelling ethical behaviour, working together, encouraging a variety of ideas, and being accountable for the value assets provide to their community.

|

Recommendation 1 We recommend all councils assess whether their governance structures and culture ensure a whole-of-council (finance, asset, and service teams) approach to asset management, including planning, operating and maintaining, disposing and monitoring performance of assets. |

Councils need complete information on all asset classes

We found 3 of the 5 councils did not have asset management plans (AMPs) for all their different classes of assets. When this is the case, councils may not prioritise infrastructure projects with the greatest need or highest value, due to having incomplete information about all assets.

Asset management plan (AMP): AMPs are long-term plans that outline the asset activities for each service.

They show that a council has plans for how it will afford to acquire, operate, maintain, renew, and eventually dispose of its assets.

For example, not having an AMP for stormwater and drainage means the council has not considered and agreed to the dates and costs of upcoming projects. This can create uncertainty around the cost and timing of other asset upgrades, such as roads. It is inefficient and more costly to dig up a newly resurfaced road to replace the stormwater drains.

The 3 councils advised they were progressively developing AMPs for all their asset classes. They said the gaps were due to:

- developing each class of asset one by one, within the limits of their resources

- drafting new AMPs to replace the previous plans, which were now out of date

- concerns about the quality of asset data, which was causing delays in having the revised AMPs approved.

Without complete asset information, councils are at risk of not receiving adequate information to support effective asset management and related investment and budgetary decisions.

|

|

Maturity self-assessment Self-assessment of ‘Information and support systems’ from our survey The state average for this element was 2.4 which is at the basic level. The basic level means that:

Note: we have not audited these self-assessments. |

Councils should assess if the data in asset management plans has changed and should be updated

None of the 5 councils assesses the information in their AMPs to see if it has changed and needs updating. This means there is a risk that, when they are making investment decisions, these councils are relying on out-of-date information about the value of their assets and when they will be due for replacement. Better practice says that AMPs are not static documents, and asset owners should revise them considering experience gained and lessons learnt by council.

If councils do not update AMPs with current data, their forecast costs for long-term capital expenditure could be inaccurate. There is an opportunity for councils to update AMPs when large changes to their assets occur, for example when there are significant and cumulative changes to cost inputs, valuation results, and updates of condition assessments. At a minimum, plans should be formally reviewed every 4 years, to align with council terms.

Councils undertake several existing activities that give them current information on their assets and could inform their decision-making. These are described below.

- Revaluations (formal valuations of assets) – Councils regularly update the value of their assets, usually on a class-by-class basis. Over a period of 4 or 5 years, councils typically have all their asset classes revalued for reporting in their financial statements. Asset revaluation provides councils with a fair value of their assets, which helps in making budget forecasts for replacement. Having accurate values for assets makes it easier to determine the cost of replacement.

- Remaining useful lives assessments – Councils annually reassess the remaining useful lives of their assets. These assessments inform budget decisions for when asset renewals will be due. This a requirement under Australian accounting standards. The estimated remaining life of an asset considers:

- physical deterioration (due to wear and tear, inadequate maintenance, damage, weathering, and decay)

- functional obsolescence (where the design of the asset is outdated and cannot handle current requirements)

- economic obsolescence (where there has been a decline in demand for services provided by the asset).

- Condition assessments – Physical engineering inspections of the condition of assets can give detailed information on the state of assets and identify maintenance solutions to reduce operating costs or improve asset life. Condition assessments are a primary input into the calculation of the remaining useful life of an asset.

- Regular safety inspections – Some types of assets undergo inspection at a set frequency to confirm they meet relevant safety requirements. Safety inspections may identify urgent unplanned maintenance work.

- Operating and maintenance activities – The regular operation of some assets can identify changes in operating and maintenance costs as assets age. In some cases, it may be more cost efficient to replace an ageing asset with a more modern option to deliver improved levels of service, with lower operating and maintenance costs.

None of the 5 councils updates asset information in its AMPs to include current information from asset valuations or other activities. This affects the accuracy of the long-term financial forecast when the asset values and renewals are summarised and aggregated. Recent increases in the costs of building materials, labour shortages, and fuel costs have also increased asset values – in some cases by as much 15 per cent in a single year. Over the 4- or 5-year life of an AMP, these increases could add up to large changes in asset values. Councils should assess the information they currently collect and refresh their AMPs to reflect any major changes to the value or condition of their assets.

Councils told us that their data on underground assets (pipes for water and sewage) is not as complete as it is for their other asset classes. However, new camera technology and inspection drones allow councils to efficiently inspect and get better information on their underground assets as well as those in remote, hard-to-reach places. Case study 2 (Figure 3C) is from a council that decided to invest in inspections to get a better understanding of the condition of its underground assets.

| Planning to collect asset condition information | |

|

Funding As part of a data verification exercise from its asset management strategy, the council planned to improve its data on the condition of its assets across all its asset classes. It allocated $3.5 million (including $1 million from a grant under the Local Government Grants and Subsidies Scheme) for the project. The council was considering replacing some of its sewers due to complaints about blockages. Asset information Prior to the inspections, council asset data showed that it had assumed the sewers:

After the inspection and condition assessments, it found that the sewers:

The inspections showed that, by increasing the level of maintenance, the council could reduce the number of blockages interrupting services. Impact Collecting data on asset condition allowed this council to improve the levels of service (reducing blockages) by increasing maintenance rather than by replacing the pipes earlier than necessary. By taking a strategic and planned approach to managing its assets, this council was able to ensure it delivered the expected level of service while optimising the total cost of owning its assets. This case study only covers the results for the sewers in a regional town with a population of less than 1,000. |

|

Queensland Audit Office, from council documents.

Councils need to improve the links between asset plans and corporate plans

Councils could not readily show us that their current mix of services supported their goals and priorities for their communities. Only one of the 5 councils had clear links in its AMPs to show how the council’s assets deliver services to achieve the goals and priorities described in its corporate plans.

Without clear alignment between all their plans, there is a risk that councils will not be able to check that their assets are delivering the level of services required to meet their corporate objectives.

All 5 councils had produced their corporate (5-year) and operational (annual) plans, as required under the Local Government Act 2009. These plans set the medium-term goals and priorities for each council’s services to the community and the immediate strategies, activities, and projects funded to achieve them.

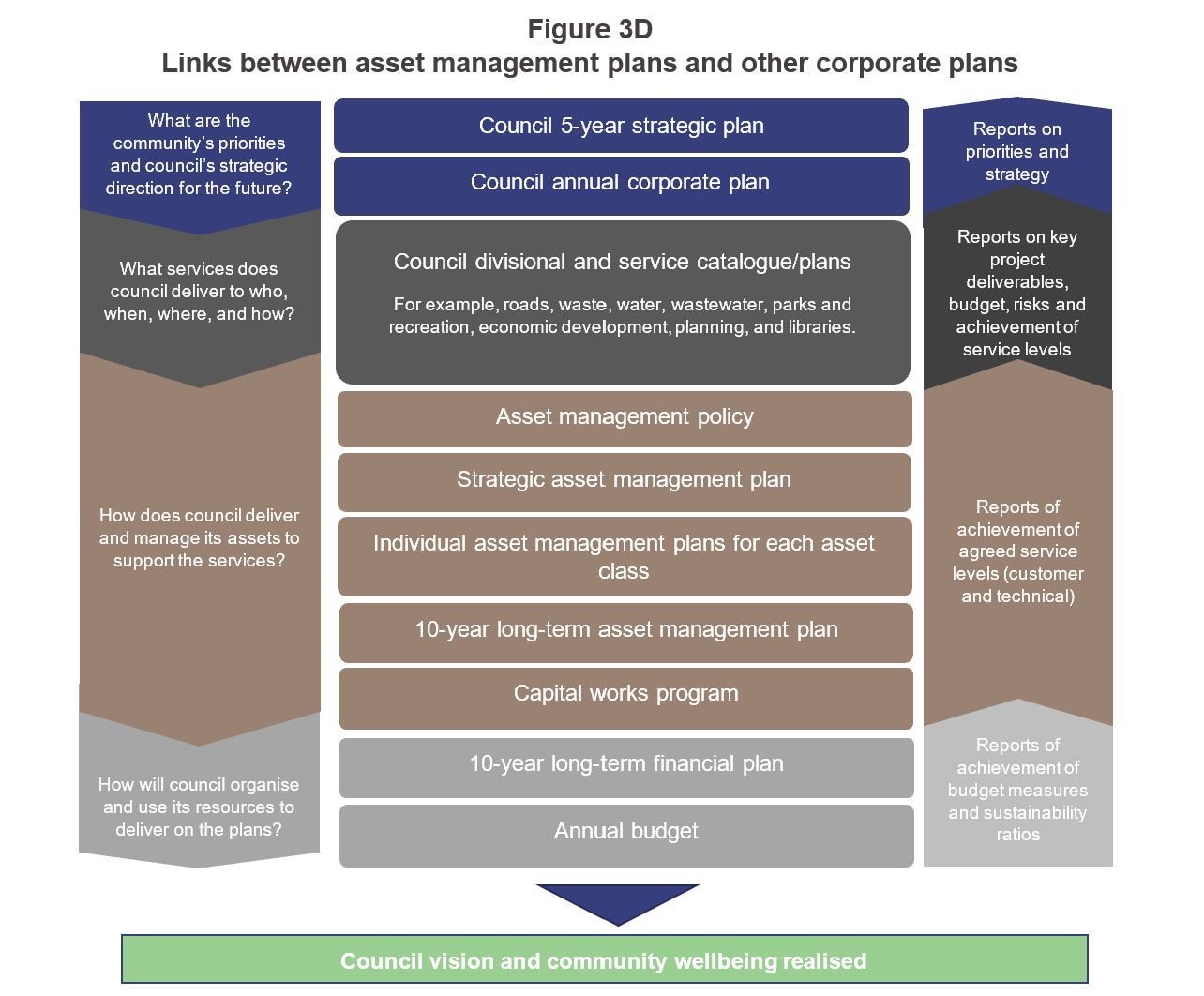

While one council had clearly included links in its AMPs to its corporate plans, the council had developed new corporate plans in 2021 and not updated its AMPs. The AMPs showed how the assets contributed to the previous corporate goals from 2016. Figure 3D shows how linking the AMPs with council’s other plans creates a clear line of sight for asset planning and achieving council’s vision for its community.

Queensland Audit Office.

Councils do not translate the community priorities from the corporate plan to the asset management objectives through the asset management policy and the strategic asset management plan. There is no clear line of sight of actionable tasks and goals in the individual asset management plans.

|

Maturity self-assessment Self-assessment of ‘Strategic planning’ from our survey The state average for this element is 2.6 which is at the basic level. The basic level means that:

Note: we have not audited these self-assessments. |

Clear alignment between AMPs and councils’ priorities for their communities (as committed to in their corporate plans) can ensure good integration across the different areas of a council. It can result in better decisions on the mix of services offered, the levels of services provided, and the overall sustainability of the services.

Better reporting on the performance of assets is needed

None of the 5 councils report internally to management or externally to the community on the performance of its assets in meeting the service levels in the plans. Without this information, councils cannot be confident that their budgets for asset renewal are at the right level to meet their communities’ expectations for the long term.

While many of the councils have targets set for service levels, they do not monitor them. For example, the water AMPs often had targets for how many days it would take to repair a leaking water main, but they do not report on how long it was taking. Without this information, management cannot intervene and reallocate resources or reprioritise renewal projects or maintenance budgets to ensure the council can meet its agreed service levels. Better information on the condition of assets and current levels of service can also inform more efficient scheduling of maintenance activities.

We found that quarterly reports to councils focused on project deliverables and activity. The reports provided no information on outcomes for the community from the councils’ services.

|

Maturity self-assessment Self-assessment of ‘Outcomes and values realisation’ from our survey The state average for this element is 1.9 which is at the aware level. The aware level means that:

Note: we have not audited these self-assessments. |

|

Recommendation 2 We recommend all councils assess whether their asset management plans are current and cover all major asset classes, including if:

|

Asset improvement plans need to have implementation time frames

All 5 councils identified improvements in their asset information and systems in their AMPs. One council engaged a consultant to develop a roadmap to outline the strategies and projects needed over the next 5 years to deliver the planned improvements. This roadmap also allocated responsibility to council staff for achieving deliverables and projects.

The other 4 councils identified various strategies to improve the individual AMPs for each asset class, but they did not set specific time frames or allocate responsibilities to council staff. Not setting time frames and accountabilities reduces the likelihood of a council achieving the desired improvements in asset management.

The benefits of developing a program plan or roadmap that clearly specifies the program of work needed to address all the gaps in councils’ asset management approaches are that:

- dependencies are clear, ensuring that a project which relies on outputs from another project does not start too early (for example, a project team should define asset data needs and determine the accuracy of its existing data before council procures a new asset management system)

- roles and responsibilities are clear, and councils understand both the scale of the planned work and how it balances with other reforms (for example, balancing planned work can help prevent organisational change fatigue, which could affect success if a council tried to implement 2 major projects, such as a new asset management system and a new payroll system, at the same time).

Asset information is stored in multiple systems

Councils were not able to readily reconcile asset information stored in multiple systems and spreadsheets to ensure it was complete and accurate. Some councils, in their response to our survey, raised concerns that data management was a challenge. They said poor data availability, data quality, and integrating their asset management system with other systems are impacting their asset management practices.

We found that 4 of the 5 councils were using multiple systems that could not share information on various asset classes. The remaining council had a single system to manage all its asset classes.

For the 4 councils, the different systems did not collect and retain standardised asset data. Having inconsistent asset data across the different systems reduces the councils’ ability to rely on their data to make informed decisions on asset projects.

Most of the councils were in the process of upgrading their asset systems. The council that had completed the transition to a single asset information system was progressively reconciling all its asset data.

Having a single or integrated asset management systems and regular reconciliation of asset information helps to:

- improve the accuracy of asset data

- increase efficiency and minimise the cost and time to search through multiple systems to find information

- improve decision-making by allowing councils to have access to accurate and up-to-date information.

When systems are not integrated or reconciled, there is a risk that assets may not be recorded, or that information on the asset may be recorded inconsistently. For example, some of the 5 councils were still identifying assets that were not previously recorded in their fixed asset registers (these were mostly of minor value).

More broadly, from our financial audits over the last 5 years we noted that on 44 occasions councils (average of 9 per year) identified ‘found’ assets they had not previously recorded in their financial statements. The total value of these assets was $1.3 billion, an average of $252 million per year. The value of assets that councils continue to find highlights the importance of having integrated systems that are regularly reconciled to identify inaccuracies.

In our survey of asset maturity, we asked councils if there were any challenges to improving their approaches to asset management. Of the 52 who responded 10 (19 per cent) said that it was difficult to integrate asset data with their existing systems.

|

Recommendation 3 We recommend all councils assess whether their data, if stored in separate asset management information systems, is recorded in a way that can be and is reconciled to the financial asset register. |

Asset management training needs to be planned and coordinated

None of the 5 councils has assessed the asset management capability of its staff and none has any formal training programs to improve asset management approaches.

The wide range of activities associated with the practice of asset management creates a risk that staff may not be able to map out a clear training program for themselves. Without a competency or capability framework for asset management, skill and awareness gaps may develop over time. Councils may not have the capabilities needed to achieve their asset management objectives.

The councils told us that it was difficult to find staff with the skills they needed and to compete with private sector wages. However, they were not effectively supporting the staff they had to improve their skills, to support their asset improvement strategies. Further information on the support provided by the department and its partners for asset management is covered in Chapter 4.

|

Recommendation 4 We recommend all councils assess whether their workforce plans and/or strategies identify the necessary asset management capabilities and the optional and mandatory training to be completed. |

|

Recommendation 5 We recommend all councils provide their assessments and associated action plans to address any of the above recommendations, where relevant, to their audit and risk committees to allow for regular progress reporting. |

4. Greater support is needed to build asset management capability

The Department of State Development, Infrastructure, Local Government and Planning (the department) administers the Local Government Act 2009 and the City of Brisbane Act 2010 (the Acts). Its role is to support local governments in being sustainable, capable, and accountable, so they can enable thriving local communities. It also administers grants for local government, which include funding for infrastructure projects.

In this chapter, we report on how effectively the department provides guidance and support to councils to develop their asset management documents.

More details are needed for how the department will support better asset management

The Local Government Sustainability and Reporting Framework (the framework), released in November 2022, does not include a clear description of how the department effectively administers the legislation to ensure compliance and support councils in improving the sustainability of the service delivered by their assets.

The department has established principles for developing sustainability indicators and developed revised draft financial sustainability measures within the financial management guidelines. However, neither the framework nor the financial management guideline outline:

- the department’s role in monitoring councils’ performance through reviewing their asset sustainability measures

- remedial action that will be taken if compliance with asset management or the asset sustainability ratios are repeatedly not met.

The framework does include the department’s role at a high level in 6 areas.

- Policy – The department, on behalf of the government, sets the primary legislative framework for the sector through the local government Acts and regulations.

- Monitoring – To support its administration of the local government Acts and regulations, the department undertakes ongoing monitoring to gather intelligence about legislative compliance, funding and capability support needs, policy and advocacy opportunities, and the overall health of the sector.

- Funding – The department develops and administers state and federal funding programs to support councils in delivering services and infrastructure to their communities.

- Capability – The department develops capability building programs to assist councils to meet their statutory responsibilities and deliver the level of performance expected by their communities.

- Performance response – The department has the power to intervene if the minister or department considers there is a significant risk to the good governance of a council.

- Advocacy – The department engages with stakeholders across and outside government at all levels to represent the interest of the Queensland local government sector.

Under its framework, the department expects councils to ensure:

- assets are well managed and maintained

- capital expenditure is adequately funded when it falls due

- projects are appropriately prioritised and costed

- councils are planning for future community needs.

The department has made it compulsory to calculate and publish the results of financial sustainability ratios (3 of which relate to assets). The 3 sustainability ratios for assets are:

- asset sustainability ratio – measures the extent to which infrastructure assets are being replaced as they reach the end of their useful lives

- asset consumption ratio – measures the extent to which infrastructure assets have been consumed compared to what it would cost to build a new asset with the same benefit to the community

- asset renewal funding ratio – indicates if a council is appropriately funding and delivering the entirety of its required capital program as outlined by its asset management plan.

The framework provides detailed explanations for the ratios and how to collect and use them. The ratios provide important information on past performance and potential threats to sustainability, but it is not clear what other information the department uses to identify councils that need support.

The department has advised us that it is developing a risk framework to interpret the results from the ratios to identify councils at a higher risk of financial unsustainability. However, it has not documented or communicated to councils the actions it intends to take to address repeated low performance. Without clear details on how it will monitor council performance, there is a risk that the sector will not achieve the desired asset sustainability ratios.

|

Recommendation 6 We recommend the Department of State Development, Infrastructure, Local Government and Planning develops a documented compliance strategy to monitor councils’ asset management approaches to meet the asset sustainability ratios. |

Advancing asset management project

As part of implementing the framework, the department developed a project to advance asset management, strengthen asset management across Queensland councils, and develop a strategy for holistically monitoring and maintaining asset management maturity across the sector.

While it is too early for us to assess the impact of this project, we observed that it includes:

- assessing the state of asset management across the sector, through a sector-wide asset management maturity survey

- developing council-specific training programs about sustainable funding, systems, resourcing, and other solutions to address capability gaps in key areas

- developing a strategy for the department to monitor and maintain council asset management capability over the long term, including developing tools and templates for councils.

Ensuring grant applications are supported by accurate information

The department administers 4 grant programs for local government that are available for infrastructure projects. It reports it has paid grants totalling $361 million over several years to June 2022. The programs are:

- Building our Regions

- Indigenous Economic Development Grant

- Local Government Grants and Subsidies Program

- Works for Queensland.

In 2022, we tabled Improving grants management (Report 2: 2022–23). This report recommended all departments assess the risk that decisions to award grants are based on incomplete or inaccurate information.

One of the ways the department could better manage and mitigate this risk would be to require councils to provide the current asset management plan for the asset class relevant to their funding application. Analysing the asset management plans could assure the department that key information on asset projects fits within councils’ long-term plans, and that any costs of operating and maintaining new assets will not affect councils’ ongoing sustainability.

|

Recommendation 7 We recommend the Department of State Development, Infrastructure, Local Government and Planning in assessing grant applications for infrastructure projects, analyses asset management plans to determine whether proposed projects are based on complete and accurate information, aligned to councils’ long-term sustainability. |

An assessment of skill gaps is needed to inform training

The department and its partners offer training workshops and online forums to discuss asset management. Participation rates are not high. Only 16 of 77 councils have taken up the training over the last 3 years. We acknowledge that councils may be accessing other training provided by other organisations such as the Institute of Public Works Engineering Australasia and the Local Government Finance Professionals. However, there is no data available on the asset management training needs in local government to allow these groups to effectively work together.

Councils and other key stakeholders in the sector have raised concerns with us about the challenges of attracting and retaining staff with adequate asset management skills. None of the 5 councils had formal asset management training programs, and none had conducted capability assessments to determine the skills required for asset management staff or to identify skills gaps.

Without ongoing asset management training to help build their asset management capability, councils are at risk of not having skilled people to plan and manage their assets. This could affect their ability to deliver services to their communities at the levels expected.

In our survey of asset maturity, we asked councils if there were any challenges to improving their approaches to asset management. Of the 52 who responded, 34 (65 per cent) said that it was difficult to attract and retain staff with the necessary asset management competencies. Councils raised concerns that they cannot compete with private sector wages for staff with good asset management skills and experience.

The department has commissioned Queensland Treasury Corporation (QTC) to provide asset management training to councils.

QTC advised that it has used the following methods to provide asset management training and support to councils over the last 3 years:

- training sessions targeting chief executive officers, finance and procurement managers, and project management teams

- tailored/customised training (specific to a council’s needs)

- webinars.

Councils’ participation in the open and tailored training programs has been relatively low, as shown in Figure 4A. Across the 3 years, 16 councils (21 per cent) have attended the open and tailored programs, while 35 councils (45 per cent) participated in the webinar events.

Most participants were from the asset management and finance teams within councils.

| Asset management training courses |

Number of councils participating |

||

|

|

2020–21 |

2021–22 |

2022–23 |

|

Open and tailored programs |

2 |

3 |

12 |

|

Webinars |

30 |

22 |

7 |

Note: The total number of councils participating across the years is not the addition of the numbers shown here as some of the same councils attended training in both 2021–22 and 2022–23.

Queensland Treasury Corporation data.

More targeted training, support, and guidance will give staff in councils access to the skills they need to complete asset management plans and keep them up to date. It can also ensure staff from across the asset, finance, and service teams have a common language and understanding of asset management concepts.

Ongoing training can also ensure councils are able to manage staff turnover and consider succession planning. Councils have an opportunity to build internal capacity by developing staff to be able to take on more responsibility as more experienced staff move on.

The department provides training and resources to new councillors on accountability, decision-making, and other responsibilities to help ensure councillors and council employees can deliver on the needs of our communities. It has also partnered with Queensland Treasury Corporation to deliver a series of free and tailored financial management workshops. The program covers financial governance and management concepts and aims to lift performance, instil strategic thinking, and raise awareness of financial management responsibilities in council. The training does not cover asset management.

In our Local government 2020 (Report 17: 2020–21) report, we recommended that the department provide periodic training to councillors and the senior leadership team for councils that have limitations raising revenue due to remoteness and small populations (that is, councils that are highly reliant on grant funding). We recommended the training focuses on helping councils:

- establish strong leadership and governance

- enhance internal controls and oversight

- improve financial sustainability in the long term.

Our recommendation aimed to improve councillors’ and senior leaders’ understanding of governance and accountability to allow them to drive change within their councils.

The international standard for asset management is clear the leadership and culture is a fundamental element for success. Without this, strategic asset management will not have the support it needs. The need for on-going training for all leaders is critical.

|

Recommendation 8 We recommend the Department of State Development, Infrastructure, Local Government and Planning works with local governments to enhance asset management capability by:

|

A better practice guide is needed to support strategic asset management for all asset classes

We found that detailed guidance to Queensland councils for key asset management planning documents is less comprehensive than that provided by entities (with responsibilities for local governments) in other Australian jurisdictions. While the department has developed a sustainability and reporting framework for local governments, it lacks the detail councils need to implement it.

The Department of Regional Development, Manufacturing and Water has developed detailed and specific guidelines for asset management planning documents for urban water service providers under the Water Supply (Safety and Reliability) Act 2008, including local governments. However, these planning documents do not apply to all asset classes owned and operated by local governments.

Guidance on integrating asset management with other planning requirements

The department’s framework takes an integrated approach to asset management, but it does not have specific guidelines to support councils in integrating their planning and reporting documents. Having integrated planning ensures a council has a consolidated list of priorities, including budget impacts, asset needs, and services to the community. It also enables:

- finance teams to access accurate information, such as when renewals or upgrades are due, and facilitates the calculation of depreciation and budgets for future capital works

- asset teams to budget for operating costs and plan maintenance activities and inspections to ensure assets are delivering the expected level of service

- service managers to report on how well the assets deliver services to the community and if new services are needed or existing services can be discontinued.

We identified gaps in councils’ asset plans that indicate they need more guidance. These gaps were explained in detail in Chapter 3.

A comparison of guidance provided by other jurisdictions shows that the department provides many of the key elements to support councils in improving their asset management. But the department does not provide enough detailed guidance on the minimum requirements for asset planning documents. It has not developed guidelines that set the minimum expectations required for a long-term asset management plan or individual asset management plans (by class). More information on the department’s framework is in Appendix F.

Figure 4B shows that, overall, Queensland compares well to other Australian jurisdictions in providing guidance to local governments on asset management, except for detailed guidance to support asset management.

| Asset management guidance | QLD | NSW | NT | SA | TAS | VIC | WA |

|

Requirements detailed in legislation |

✓ |

✗ |

✓ |

✓ |

✓ |

✓ |

✗ |

|

Integrated framework for asset management |

✓ |

✓ |

✗ |

✗ |

✓ |

✓ |

✓ |

|

Detailed guidelines/handbooks to support asset management |

✗ |

✓ |

✗ |

✗ |

✓ |

✓ |

✓ |

|

Reporting requirements for asset sustainability |

✓ |

✗ |

✗ |

✗ |

✓ |

✓ |

✗ |

Note: QLD – Queensland; NSW – New South Wales; NT – Northern Territory; SA – South Australia; TAS – Tasmania; VIC – Victoria; WA – Western Australia.

Queensland Audit Office analysis of national guidelines and frameworks.

The Victorian Local Government Asset Management Better Practice Guide is very detailed, and it highlights the benefits of effective asset management. Importantly, it also lists the key elements of 3 critical documents: the asset policy, strategy, and plan. It explains why each of the documents is important and what information to include.

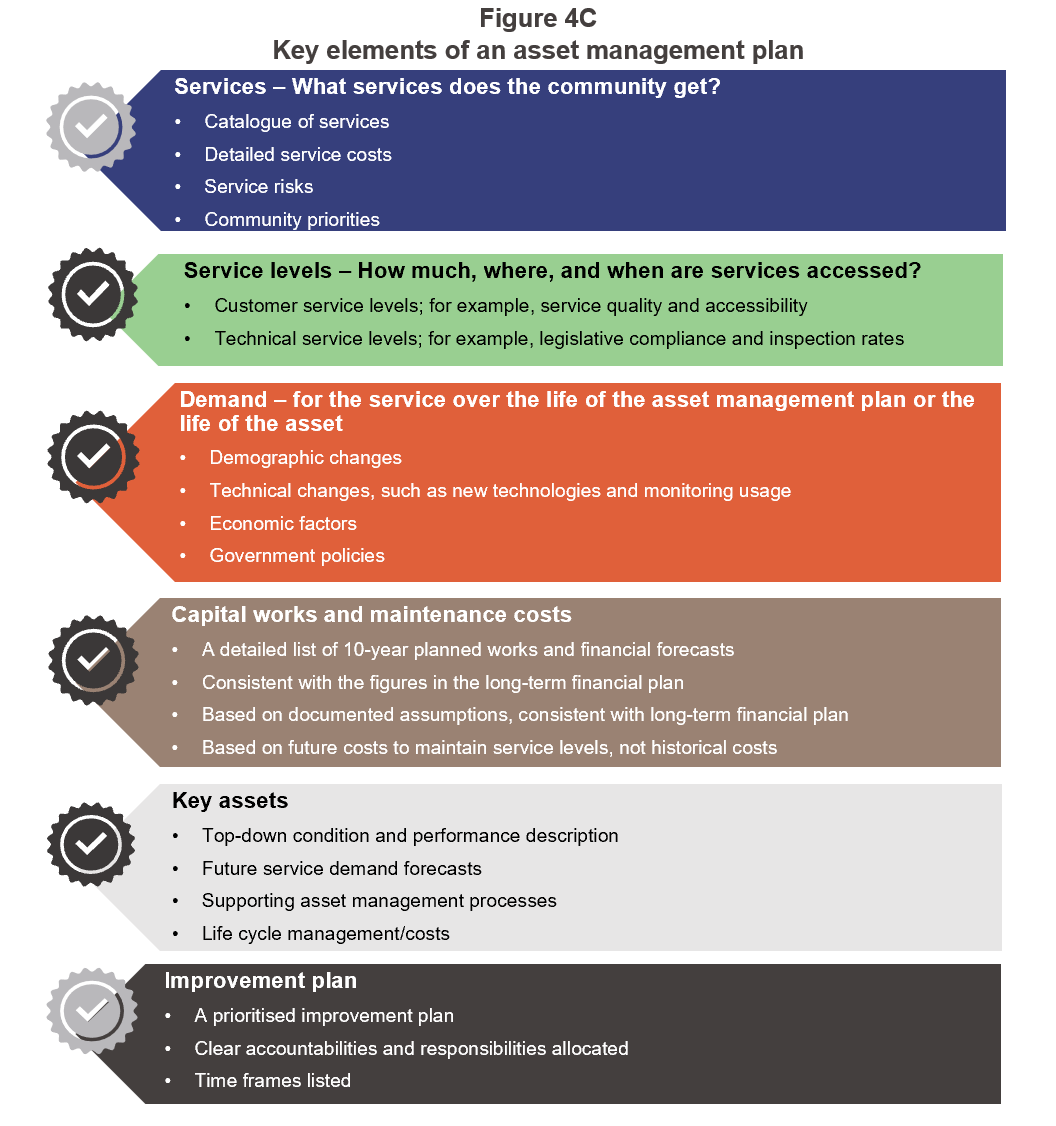

Figure 4C shows the key sections of an AMP and details some of the critical elements that councils need further support and guidance to meaningfully complete. Involvement of the finance, assets, and service teams is vital for developing a useful AMP that integrates with councils’ other key plans. The Victorian better practice guide encourages councils to take a strategic approach to developing asset management plans that include:

- engaging with community on the trade-off between cost, service levels, risks, and social equity

- managing and communicating risk and affordable service targets

- developing long-term plans for financial sustainability

- providing affordable service level objectives that include a balanced scenario considering performance, cost, and risk

- integrating the effective management of assets with service planning.

Queensland Audit Office based on better practice.

Without clear guidance, Queensland councils may not be able to demonstrate integration between their asset plans with whole-of-council planning or consistently document how they will manage assets to deliver services in the long term. This could lead to reduced service delivery to their communities.

|

Recommendation 9 We recommend the Department of State Development, Infrastructure, Local Government and Planning develops comprehensive better practice guidance for local government on the minimum requirements and templates for the following key asset management documents:

|