Overview

State and local government owned water entities provide water throughout Queensland, to households, agriculture, mining, electricity generation, tourism, and manufacturing industries.

Tabled 28 January 2021.

Report on a page

This report summarises the audit results of six entities in Queensland’s water sector: Seqwater, Sunwater, Urban Utilities, Unitywater, Gladstone Area Water Board, and Mount Isa Water Board.

Liabilities from the 2011 South East Queensland floods class action

Seqwater’s financial statements should have included a liability and expense as a result of an unfavourable court judgement relating to the 2011 South East Queensland floods class action. We assessed this unrecorded liability and expense to be of significant value. Sunwater appropriately recorded its share of the liability and expense, at $330 million.

Financial statements are reliable

Apart from this non-recorded liability and expense, all entities’ financial reports are reliable and comply with relevant laws and standards. They were prepared in a timely manner and were of good quality.

Information security continues to be a challenge

This year, we identified more weaknesses in the systems and processes (internal controls) entities use to prepare financial statements. Security of information systems is an issue in four of the six entities, and continues to be the most common weakness across the public sector.

Profits and shareholder returns have declined

The combined profit of the sector was reduced by the liability related to the class action. As a result, shareholder returns were lower than in previous financial years.

Continuing asset improvement programs involving significant infrastructure investment are likely to impact on the sector’s returns to shareholders over the next decade.

Drought and the need to provide a sustainable supply of water are posing challenges

The sustainable supply of water continues to be a challenge for the sector, with the majority of Queensland in drought—particularly South West Queensland. Extreme weather conditions increase operating costs and the need to prioritise water security projects.

Recommendations for entities

We have identified the following recommendations:

Strengthen the security of information systems (all entities) |

|

|

We recommend all entities strengthen the security of their information systems. They rely heavily on technology, and increasingly, they have to be prepared for cyber attacks. Any unauthorised access could result in fraud or error, and significant reputational damage. Their workplace culture, through their people and processes, must emphasise strong security practices to provide a foundation for the security of information systems. Entities should:

Entities should also self-assess against all of the recommendations in our report—Managing cyber security risks (Report 3: 2019–20)—to ensure their systems are appropriately secured. |

|

Improve timely recognition of donated assets (distributor-retailers) |

|

|

Distributor-retailers (Urban Utilities and Unitywater) need to:

|

|

Understand complex employee arrangements (all entities) |

|

| REC 3 | As part of the negotiation process for enterprise agreements, entities should ensure they understand how these arrangements interact with employee contracts. |

1. Overview of entities in this sector

Notes:

- Seqwater, Sunwater and the water boards also directly supply water to local councils who operate their own retail businesses. Like distributor-retailers, these local councils on-sell water to households or industries. Local councils are excluded from this report.

- South East Queensland (SEQ) customers refers to household and industry customers in the Brisbane, Ipswich, Somerset, Lockyer Valley, Scenic Rim, Moreton Bay, Sunshine Coast and Noosa council areas.

- Category 1 water boards are for-profit authorities established under the Water Act 2000. GAWB—Gladstone Area Water Board; MIWB—Mount Isa Water Board.

- Category 2 water boards are other not-for-profit authorities and are outside the scope of this report.

- Responsibility for regulation of the safety of referable dams, management of state-owned dams and weirs, and oversight of Category 2 water boards transferred from the former Department of Natural Resources, Mines and Energy from 12 November 2020.

Compiled by the Queensland Audit Office.

2. Results of our audits

This chapter provides an overview of our audit opinions for each entity in the water sector. It also provides conclusions on the effectiveness of the systems and processes (internal controls) entities use to prepare financial statements.

Chapter snapshot

Audit opinion results

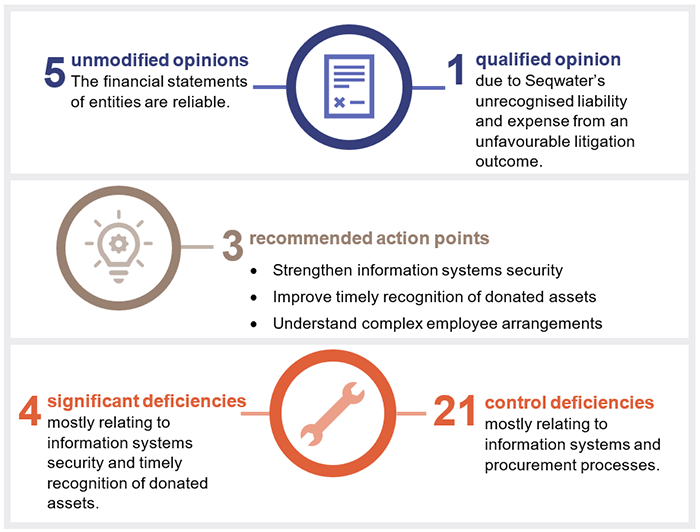

We issued unmodified audit opinions for five of the six water entities. Seqwater received a qualified opinion for not recording a liability and matching expense as a result of the unfavourable court judgement relating to the 2011 South East Queensland floods class action.

All entities met their legislative deadlines, and readers can rely on the results in the audited financial statements (except for the qualification on Seqwater’s financial statements, meaning its profit was overstated). The audit opinions we issued are listed in Appendix C.

We express an unmodified opinion when financial statements are prepared in accordance with the relevant legislative requirements and Australian accounting standards.

We express a qualified opinion when financial statements are fairly presented, with the exception of a specified area.

Liabilities from the 2011 South East Queensland floods

A class action relating to the 2011 South East Queensland floods was brought against Seqwater, Sunwater, and the Queensland Government through the Supreme Court of New South Wales (the Court). A judgement was handed down in favour of the plaintiff in November 2019 and the Court determined the percentage of liability to be allocated between Seqwater (50 per cent), Sunwater (30 per cent) and the Queensland Government (20 per cent) in May 2020. Both Seqwater and Sunwater are appealing the judgement and have insurance policies that apply to this situation.

The judgement created a financial obligation for the group members that can be estimated and is likely to require payment. Under the accounting standards, Seqwater should have recognised a liability and a matching expense. Sunwater has appropriately recognised a $330 million liability and expense.

Audit opinion issued since our last report

We previously reported that the Gladstone Area Water Board was granted an extension for finalising its 2018–19 financial statements. We subsequently issued an unmodified opinion for these financial statements on 13 November 2019.

The Gladstone Area Water Board’s current directors were unable to sign the 2018–19 financial statements in a timely manner due to the timing of their appointment. They had not been in their positions during that whole financial year. The former directors exceeded their terms by an average of two years and continued to hold office until new directors were appointed. We will examine board appointment processes across the Queensland Government in our planned 2020–21 report on appointing and renewing government boards.

Entities not preparing financial statements

Not all Queensland public sector water entities produce financial statements. Appendix D provides a full list of those not preparing financial statements, and the reasons.

Mature financial statement preparation processes are in place

We worked with the water entities as they undertook a self-assessment of their financial statement preparation processes using the maturity model on our website. They assessed the majority of their processes as ‘integrated’ or ‘optimised’—the highest levels of maturity. This means that they have assessed that their processes supporting the preparation of financial statements are efficient and provide high quality information in a regular, timely manner.

Most entities identified an opportunity to further automate the preparation of financial statements. Nevertheless, the common electronic spreadsheets and word processing tools they currently use are still fit for purpose. The entities recognise that they need to balance the cost of investing in automation against the benefits to be derived.

Internal controls are generally effective

We assessed whether the systems and processes (internal controls) entities use to prepare financial statements are reliable. We have reported any deficiencies in the design or operation of those internal controls to the management of the entities for their action. The deficiencies are rated as either significant deficiencies (those of higher risk that require immediate action by management) or deficiencies (those of lower risk that can be corrected over time).

Overall, we found the internal controls water entities have in place to ensure reliable financial reporting are generally effective but could be improved.

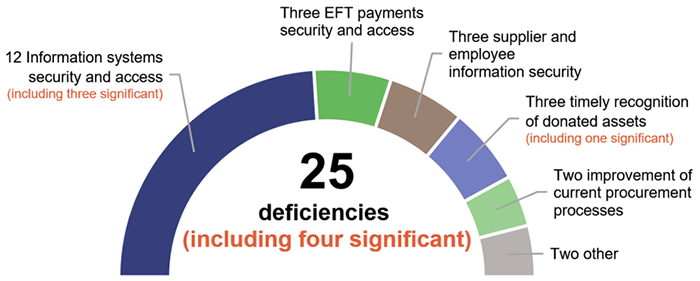

In 2019–20, we reported four significant deficiencies and 21 deficiencies in internal controls across the sector. Figure 2A shows the types of deficiencies we identified.

Note: EFT—electronic funds transfer.

Compiled by the Queensland Audit Office.

We have received responses from each entity on their planned corrective action to the internal control issues raised. We are satisfied with the responses and proposed implementation time frames.

Strengthen information systems security and access

Water entities rely on information technology systems to operate their business and prepare financial statements, so they must have strong controls over who has access to the systems and the information within. Weaknesses in information technology controls increase the risk of undetected errors or potential financial loss, including fraud.

For some years, the most common internal control weakness across the public sector has been the security of information systems. This year, we recommended four of the six water entities strengthen the security of their information systems. They are not the only ones who need to do this.

All entities across the public sector need their people and processes to have strong security practices—so that information systems are promptly updated, to respond to changes within their entity and remain protected from external threats.

This year there has been a significant and sustained increase in external attacks, as cyber criminals attempt to take advantage of changes in working arrangements necessitated by the COVID-19 pandemic. This has emphasised the importance of secure information systems.

Recommendation for all entitiesStrengthen the security of information systems (REC 1) |

|

We recommend all entities strengthen the security of their information systems. They rely heavily on technology, and increasingly, they have to be prepared for cyber attacks. Any unauthorised access could result in fraud or error, and significant reputational damage. Their workplace culture, through their people and processes, must emphasise strong security practices to provide a foundation for the security of information systems. Entities should:

|

Improve timely recognition of donated assets

Distributor-retailers collect infrastructure charges (developer contributions) from developers. These are calculated based on the size and type of development. Developer contributions are settled through cash contributions or donated assets (for example, water and sewerage infrastructure). These contributions are intended to increase the capacity of the water and sewerage networks that are needed to support new developments. They are reported as revenue by the distributor-retailers when a connection certificate is issued for completed works that are compliant with laws and regulations.

Recognition of revenue from donated assets is affected when developers are late in submitting engineer-certified drawings or when the values are inaccurate. As a result, the revenue and assets may be recorded in the incorrect period or not at all.

We noted the following control weaknesses affecting the timely recognition of donated assets:

- unrecorded assets that had been constructed but were waiting for a connection certificate

- missing engineering drawings for issued connection certificates

- delays in processing the engineering drawings.

Details on the trend of developer contributions and building approvals are provided in Appendix E.

Recommendation for distributor-retailersImprove timely recognition of donated assets (REC 2) |

|

Distributor-retailers need to:

|

Understand complex employee arrangements

In 2019–20, Sunwater and Seqwater became aware that several employee entitlements (for example, salaries, superannuation, and overtime) may be covered by both individual employment contracts and enterprise agreements. Due to the legal complexity of the interactions between the relevant enterprise agreements and the employee contracts, some employee entitlements may have been underpaid.

As at 30 June 2020, Sunwater and Seqwater increased employee entitlements by $5.3 million and $1.6 million respectively, covering current and former employees (inclusive of other associated costs, for example, payroll tax). In respect of Seqwater, those additional employee entitlements do not include the interaction between the relevant enterprise agreements and employment contracts because they are still assessing the arrangements. They expect to resolve this matter in 2020–21.

Recommendation for all entitiesUnderstand complex employee arrangements (REC 3) |

|

As part of the negotiation process for enterprise agreements, entities should ensure they understand how these arrangements interact with employee contracts. |

3. Financial results and challenges

This chapter analyses the key financial results and challenges faced by the sector.

Chapter snapshot

Sustainable profits and shareholder returns

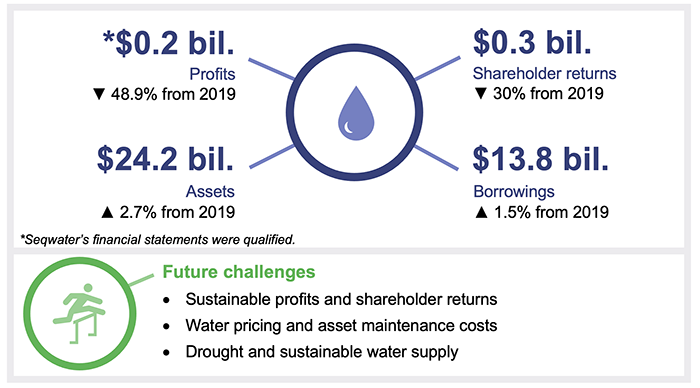

The water sector’s profits decreased by 48.9 per cent in 2019–20 (see Figure 3A). The largest impact to the sector’s profits was the $330 million expense and matching liability recognised by Sunwater arising from the class action. By Seqwater not recognising its share of the expense (and associated liability), the sector’s reported profits for 2019–20 were higher than they should be. Returns to the Queensland Government were lower than in previous financial years due to the sector’s reduced profit. Seqwater and Sunwater hold insurance policies relevant to the class action, but may need to raise additional funding if they are unable to meet their class action liability when payment is required. The sector’s total shareholder returns of $294 million are made up of dividends, participation returns and income tax equivalents. Details on financial flows to and from government are provided in Appendix I.

The sector was not directly affected by the financial impact of COVID-19, but it extended assistance to its customers to help with their water bills through interest-free payment extensions, flexible payment plans, and suspended price increases.

Water pricing and asset maintenance costs

In response to COVID-19, the Queensland Government decided in May 2020 to set rural irrigation water prices for 2020–21 at 2019–20 levels or to pass on any price reductions recommended by the Queensland Competition Authority. The Queensland Government also confirmed that it will continue to absorb irrigators' share of dam safety costs as a longer-term price policy setting, rather than seek to recover these costs through irrigation prices. The 2020–21 Queensland Budget also committed $81.6 million over the next three years to support irrigators where it sets the prices for water provided by Sunwater and Seqwater. Commencing from 1 July 2021, this funding will include a 50 per cent discount on irrigation prices for fruit and vegetable growers and a 15 per cent discount for all other irrigators.

Drought and sustainable water supply

Queensland has been experiencing extreme weather conditions, with 41 councils drought declared (67.4 per cent of the state). Prolonged drought has led to reduced water storage levels, increased operational costs, and the need for increased capital investment in water security projects. Details of drought-declared areas are provided in Appendix F.

Maintaining water supply in South East Queensland

Seqwater’s Water Security Program includes drought responses that are triggered when the combined total of the region’s 12 major dams reduces to predetermined levels.

Seqwater’s drought response was triggered in November 2019, when dam levels fell to 60 per cent. In 2019–20, the Gold Coast Desalination Plant doubled water production to 13,804 megalitres (28.4 per cent of its total capacity) to the South East Queensland water grid, increasing the plant’s operating and maintenance costs to $19.3 million (an increase of 5.9 per cent from 2018–19).

Seqwater, in consultation with the Queensland Government, deferred the decision to fully restart the Western Corridor Recycled Water Scheme until after the 2020–21 summer. This was because rainfall received over February 2020 added more than 10 per cent to the South East Queensland water grid and the Bureau of Meteorology forecasted increased rainfall over the summer. The scheme’s assets therefore largely remained in ‘care and maintenance’ mode (were not used) throughout 2019–20, however, it produced water for industrial customers, such as power stations, to reduce the draw down on drinking water storages.

Dam improvement programs and safety regulation

Each dam owner is responsible for dam improvements and must ensure they manage safety risks in accordance with the provisions of the Water Supply (Safety and Reliability) Act 2008. The Department of Regional Development, Manufacturing and Water is the safety regulator (responsibility transferred from the former Department of Natural Resources, Mines and Energy from 12 November 2020) and in 2020–21 we plan to prepare a report to parliament on the effectiveness of its regulation.

Sunwater and Seqwater regularly monitor and assess their dams. They can be decades old, so improvement programs are critical in bringing underlying infrastructure in line with current design and safety standards. The dam owners’ assessments aim to maintain public safety and secure water supply while delivering value for money.

Dam improvements are a significant cost to entities and are funded through additional borrowings, funding from the state or federal government, and current and future water prices.

Paradise Dam, located south-west of Bundaberg, is owned by Sunwater. In April 2020, a Commission of Inquiry into Paradise Dam safety released its final report. The report notes uncertainties regarding the dam’s construction. In May 2020, work started on lowering the dam wall by 5.8 metres to improve its stability and the safety of downstream communities while the best, long-term solution is developed.

Appendix G provides details of significant dam improvement programs for Seqwater and Sunwater.

Infrastructure projects to ensure sustainable water supply

The sector has several projects underway to address the issue of water supply in drought areas across Queensland. For communities that are experiencing severe drought, interim solutions are in place to help them receive continuous supplies of water.

For example, Southern Downs Regional Council continues to have severe water restrictions of 120 litres per person per day. Stanthorpe has relied on full-time water carting (costing about $800,000 a month), since the Storm King Dam levels decreased in January 2020.

Long-term water security projects include the:

- Rookwood Weir Project—Construction has begun on a weir that will provide up to 76,000 megalitres (ML) of extra water supply and provide opportunities for increased agricultural and industrial development in Central Queensland, and boost urban water security for the Livingstone and Gladstone communities.

- Haughton Pipeline Duplication Project—Construction continues for a duplicate pipeline for the Townsville area.

- Granite Belt Irrigation Project—Pre-construction activities have begun for a dam at Emu Swamp for the Stanthorpe area.

All other long-term water security projects are in the early stages of planning or feasibility studies. These projects are important to ensuring sustainable water supply during drought, but they take significant time and resources to plan and construct.

The sector’s returns to shareholders are likely to be impacted as asset improvement programs continue to involve significant infrastructure investments.

2020 water dashboard

This Queensland Audit Office interactive map of Queensland allows you to explore the financial performance of the state's water entities, and view storage levels, the number of dams, and drought declared areas across the state. You can find information on your water services by typing your address into the search bar or clicking on your local council.