The new standard AASB 16 Leases was issued over two years ago, in February 2016. The broad intention of the standard is to put ‘off‑balance sheet’ operating leases ‘on-balance sheet’.

This standard will significantly affect lessees, but accounting is largely unchanged for lessors. Intermediate sub-lessors (those that act as lessee and then lessor for the same asset) are also likely to be affected.

For lessees, the accounting will initially seem familiar. However, this may give people a false sense of security, as the detailed calculations are different.

At a high level, the accounting is based on finance lease accounting. You determine the term of the lease, considering the potential exercise of option renewals. Then you determine the future lease payments. Following this, you recognise the discounted future lease payments as a lease liability. Lease payments are split between interest expense and reduction of liability. For the leased asset, you recognise a right-to-use asset at the same amount of the lease liability. The leased asset is then depreciated over the life of the lease.

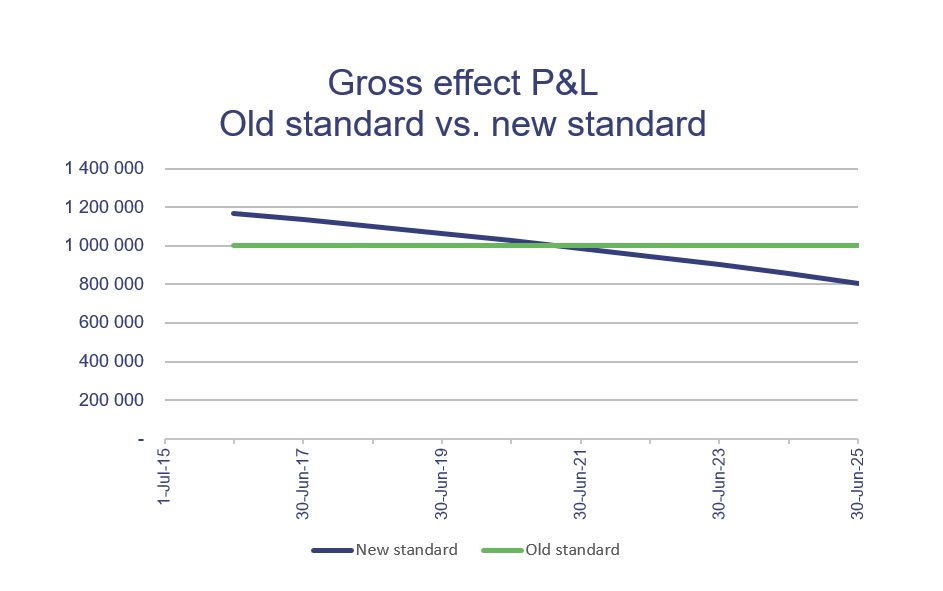

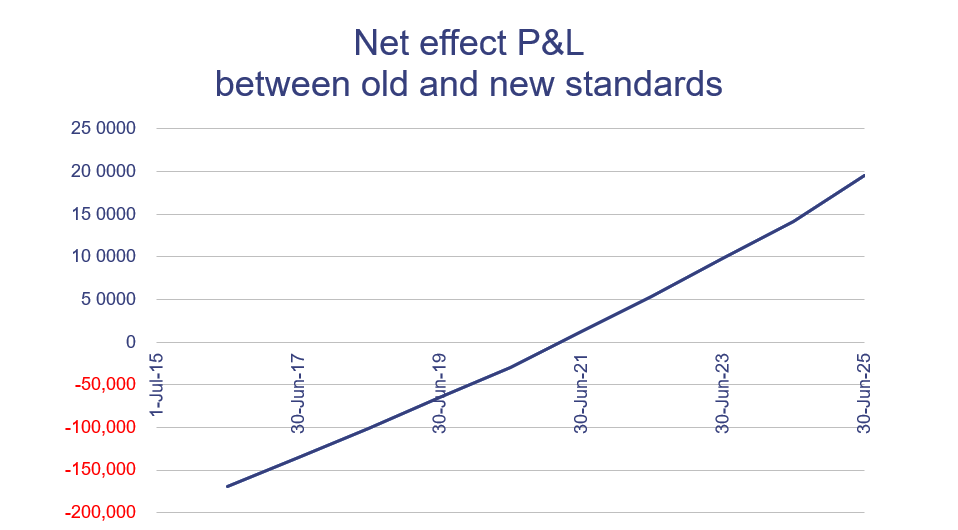

While most discussions on the effect of the new standard focus on the higher liabilities and higher assets recognised, profit/surplus is also affected. Under the new standard, you get a financing effect. At the start of the lease, you have a higher interest expense because of the higher liability, as well as the straight-line depreciation. Therefore, this means a higher combined expense and lower profit than recognising lease payments as an expense. Then later, the profit effect flips so the lease accounting expense is lower than the lease payments.

The following charts compare expense under the new standard to the old standard, firstly on the effect of the gross expenses, and next the effect on net profit. In this example, we have used an operating lease of $1 million per annum fixed (paid monthly in arrears) and a 10-year lease term. We used a 5 per cent discount rate to see the impact of the new standard.

However, there is some good news. There is relief from the new accounting for small value items and for leases with terms less than 12 months. While small value is not defined, it is usually linked to existing asset recognition thresholds. This will mean that items such as PCs and mobile phones will not usually not be caught.

In a related article, we discuss the complexities around the detailed accounting for consumer price index and other lease rental adjustments (for example, market reviews).

You should familiarise yourself with the new standard and understand how it will affect you. You should also start collecting the necessary data for the calculations. The extent of the data collection will depend on how sophisticated your current lease management system is, and the complexities of your lease rental adjustments and option renewals.

Related article