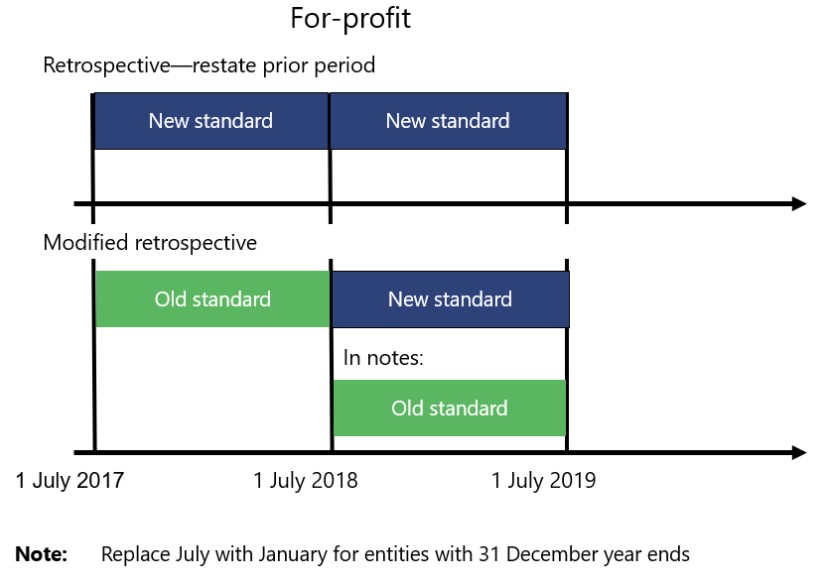

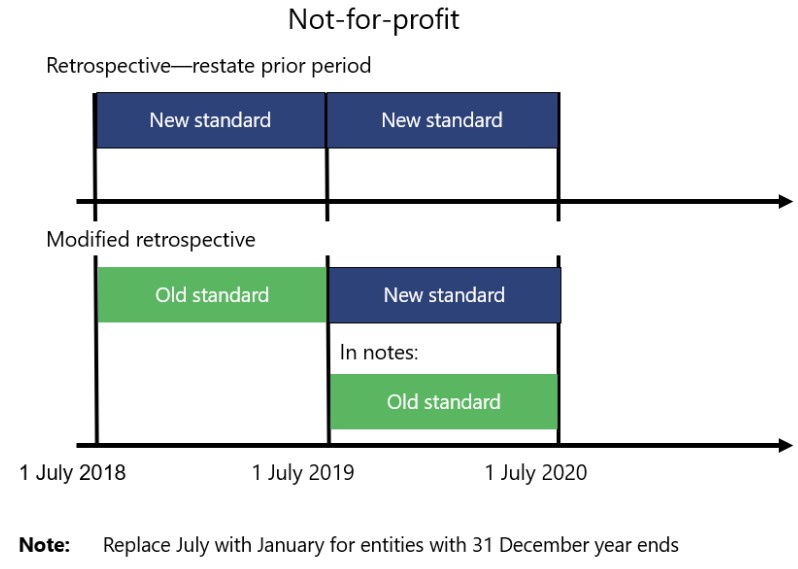

AASB 15 applies to both for-profit and not-for-profit entities. For-profit entities must apply AASB 15 for financial years beginning on, or after, 1 January 2018. Not‑for-profit entities have another year to get ready and must apply AASB 15 for financial years beginning on, or after, 1 January 2019.

A critical issue when first applying AASB 15 is determining which of two transition methods to use – the fully retrospective method or the modified retrospective method (also referred to as the cumulative catch-up method). This decision determines the extent of comparative disclosures and may not be the accountant’s choice to make. The choice may be made by the board or by the body that sets your reporting requirements.

AASB 15 includes the usual transition method of fully restating comparatives to the new method. Therefore, when preparing financial statements for the financial year beginning on, or after, 1 January 2018 (for-profit), or on, or after, 1 January 2019 (not-for-profit), you will need to also restate the previous financial year.

AASB 15 includes an alternate modified retrospective method that does not require the prior period restatement. However, you will need to disclose what the current year would have been under the old system. This is different to the transition method of other standards, where the old system is no longer required after the new standard commences. For those of you subject to Queensland Treasury’s Financial Reporting Requirements, this method is currently being proposed.

The following charts show the timing differences between for‑profit and not-for-profit for transitioning to AASB 15 for each of the for-profit and not-for-profit starting dates.

AASB 1058 Income for NFPs – transition

AASB 1058 has similar transitional provisions and the same transition dates for NFP entities. Applying the two standards, and their interaction, can be complex.

The AASB has provided further transitional relief for NFP entities. These include:

- not having to restate arrangements that were recognised up-front under AASB 1004 and revenue deferred under AASB 15

- not having to restate arrangements where the consideration paid for an asset was above nominal consideration but was ‘significantly less than fair value’.

The above relief does not apply to leases, including what are currently classified as operating leases, with significantly below-market terms and conditions. This includes peppercorn leases. The AASB has included specific provisions to fair value these leases.

Revenue – the Five Step Model for AASB 15

AASB 15 applies to both for-profit and not-for-profit entities. For-profit entities must apply AASB 15 for financial years beginning on, or after, 1 January 2018.