Overview

The Queensland Government established the Queensland Future Fund in 2020 to offset the state's debt. It provides the structure under which individual funds can be created to hold assets for managing the state's debt or for other purposes.

Tabled 13 December 2021.

Report on a page

The Queensland Future Fund was established to offset the state’s debt

The Queensland Future Fund was established in 2020. The Queensland Future Fund is a framework under which funds may be created. The first of these funds, the Debt Retirement Fund, was established this year. The underlying assets supporting the Debt Retirement Fund are held in several investment trusts. Investments and returns from the Debt Retirement Fund can only be used to reduce state debt. The establishment of the Queensland Future Fund and its Debt Retirement Fund impacted the investments and assets of several government entities. Each entity has reported on its individual financial impacts, but the overall impact across government is not captured in one place. This could be addressed by having separate financial statements for the Queensland Future Fund. Separate financial statements would be comparable to practices in other jurisdictions (such as New South Wales).

Assets contributed to the Debt Retirement Fund

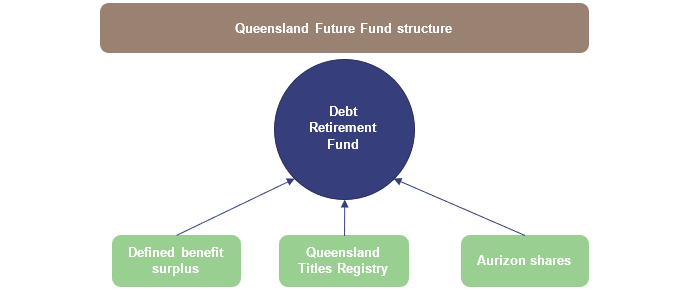

The government transferred assets valued at $7.7 billion into the Debt Retirement Fund in 2020–21. They included the Queensland Titles Registry business (which manages the land and water titles registries in Queensland and collects fees for managing these registries), shareholdings in Aurizon (formerly QR (Queensland Rail) National), and surplus assets from the defined benefits fund (investments held to meet future superannuation obligations and other long-term liabilities of the state). Not all of the ownership of the Queensland Titles Registry was included in the Queensland Future Fund. Twenty-five per cent of the returns from the Queensland Titles Registry will be used to deliver three initiatives.

Subsequent changes to assets owned by the fund

After the establishment of the Debt Retirement Fund, QIC Limited sold a portion of the Aurizon shares. On the same date as the Queensland Titles Registry business was transferred in, part of the ownership in it was transferred to government superannuation assets and a statutory body in exchange for other more liquid investments. A $2.1 billion loan was also taken out against the Queensland Titles Registry business. This was to provide liquidity to the fund and support the state’s credit rating. On 30 June 2021, the Debt Retirement Fund had a value of $7.7 billion, which is reported in Queensland Treasury’s financial statements and the Report on State Finances.

Impact on the Queensland Titles Registry

The Queensland Titles Registry shifted from being part of a government department to being a separate company, owned indirectly by multiple government entities. This move was completed through the passing of the Queensland Future Fund (Titles Registry) Act 2021. Employees transferred with the business and can choose to move back to the public sector for a period after this move. The ownership of the business could continue to change over time.

It is too early to determine if the fund has met its objectives

The Treasurer set out the objectives of the fund in the 2021–22 state budget. The fund met the objective of having assets of $7.7 billion as at 30 June 2021 and improving the net debt to revenue ratio for the state. Other objectives will be measured in the medium to long term.

1. Recommendations

Introduce a statutory requirement for the Treasurer and Queensland Treasury to prepare annual financial statements and provide additional information for funds established under the Queensland Future Fund Act 2020 |

|

|

In our State finances 2020 (Report 15: 2020–21) report to parliament, we recommended that Queensland Treasury amend the Queensland Future Fund Act 2020 to include a requirement for financial statements to be prepared, audited, and made publicly available for each fund created under the Act. This recommendation was made based on practices seen in other jurisdictions (such as New South Wales) for their future funds. This recommendation was not accepted. Based on the transactions that occurred within the Queensland Future Fund structure in 2020–21, and the information publicly available on these transactions, we recommend that the Treasurer and Queensland Treasury reconsider this recommendation. Provision of further information would provide information on the activities of the Queensland Future Fund and its investments for the public and assist in the measure of a ‘transparent and open government’. Specifically, we recommend the Queensland Future Fund Act 2020 be amended to require:

|

Reference to comments

In accordance with s. 64 of the Auditor-General Act 2009, we provided a copy of this report to relevant entities. In reaching our conclusions, we considered their views and represented them to the extent we deemed relevant and warranted. Any formal responses from the entities are in Appendix A.

2. The Queensland Future Fund

This chapter covers the establishment of the Queensland Future Fund, outlines the assets that were initially transferred into it, and explains what has happened to those assets since.

Establishing the fund

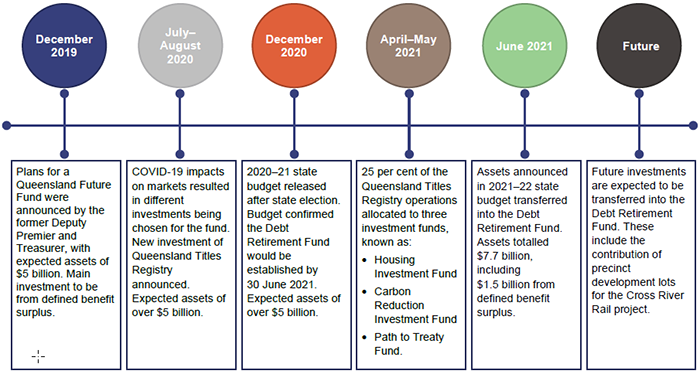

In December 2019, the former Deputy Premier and Treasurer announced plans for a Queensland Future Fund. Its design was based on the NSW Generations Fund.

The Queensland Future Fund was established in August 2020 under the Queensland Future Fund Act 2020, which outlines the administration, oversight, and reporting required. It also creates a new category of assets, known as ‘prescribed’ assets, which must always be held in state ownership. Any assets not included as a prescribed asset may be externally owned.

The Queensland Future Fund is not an investment fund in itself. It provides the structure under which individual funds can be created to hold assets for managing the state’s debt or for other purposes. The first individual fund set up under this structure is the Debt Retirement Fund. The underlying assets supporting the Debt Retirement Fund are held in several investment trusts. The assets and returns from the Debt Retirement Fund can only be used to reduce the state’s debt.

Appendix B provides details of the legislation that passed through parliament to set up the Queensland Future Fund.

Further details of the fund were provided in the 2021–22 state budget. Figure 2A outlines the Queensland Future Fund structure and the assets the government announced for the Debt Retirement Fund in the budget.

Compiled by the Queensland Audit Office.

Managing the Queensland Future Fund and its Debt Retirement Fund involves several entities across government, as shown in Figure 2B.

Compiled by the Queensland Audit Office.

Establishing the Debt Retirement Fund

Figure 2C shows the main steps involved in establishing this fund.

Compiled by the Queensland Audit Office.

Assets initially transferred into the fund

Figure 2D identifies the assets the government contributed to the Debt Retirement Fund. QIC Limited manages these assets on behalf of the state and was involved in the transfer process.

Compiled by the Queensland Audit Office.

Transfer and valuation of the Queensland Titles Registry

The Queensland Titles Registry is responsible for the registration of all land‑related transactions in Queensland. It also operates other registries including water allocation, foreign land ownership and leasehold registers. In managing these registers, it collects fees for changes to, or searches of, the registers.

The Queensland Titles Registry operations were transferred from the Department of Resources into a company called Queensland Titles Registry Pty Ltd on 18 June 2021. On this date, the Debt Retirement Fund took ownership of 75 per cent of the company, and the state’s Consolidated Fund (through three funds) held 25 per cent. QIC Limited currently manages the operations of the Queensland Titles Registry.

The transfer of the Queensland Titles Registry operations included all assets and liabilities of the operations, as well as employees and employee entitlements. The new owners have the right to the revenue collected by the Queensland Titles Registry for the next 50 years. Future rates charged for registry services are capped under legislation and must be notified to the state (and the public) prior to the start of each financial year.

Those employees who transferred retained the entitlements of the state award under which they were employed, and can choose to return to the public sector within a specified period.

Because the transfer of the Queensland Titles Registry did not involve a public sale, market data was not as readily available as it would be for other asset sales. As a result, the valuation of the Queensland Titles Registry was determined in a process involving external valuers.

The Queensland Titles Registry was valued at $7.98 billion at 30 June 2021. This value was calculated through a discounted cash flow over 50 years. (A discounted cash flow is used to estimate the future income for the period for which the rights to the revenue are held, in today’s dollars.). The Debt Retirement Fund received $6 billion of this value.

The value was higher than initial estimates and that of titles registries in other states due to the length of time the arrangement covers and the inclusion of property value based transaction fees (a different fee structure compared to other states).

Appendix C details the process flow of this transaction.

|

Creation of three investment initiatives When the 2021–22 state budget was presented to parliament, the value of the Queensland Titles Registry was higher than initial estimates. The government announced it would contribute value greater than the $6 billion included in the Debt Retirement Fund to three new funds, outside of the Queensland Future Fund structure. The three funds will be used to fund long-term priorities, including:

Returns from the Queensland Titles Registry are allocated to these three initiatives based on their funding allocation above. These funds were not established under the same legislation as the Queensland Future Fund. These investments are held within the state’s Consolidated Fund. The creation and establishment of these investment funds will be further explained in our state finances 2021 report. |

Surplus assets from the defined benefit fund (government superannuation assets)

The state holds investments to cover the costs of meeting defined benefits for the State Public Sector Superannuation Scheme (QSuper). Historically, the value of these investments has exceeded the value of the defined benefit obligation, resulting in a surplus.

When announcing plans for the Queensland Future Fund in December 2019, the government expected the defined benefit surplus would be up to $5 billion. However, due to the initial impact of COVID-19 on markets, this surplus reduced. Ultimately, $1.5 billion was transferred from the defined benefit surplus before 30 June 2021. The defined benefit scheme remained in surplus after this transfer. Under the legislation which established the Queensland Future Fund, the defined benefit fund is required to be fully funded.

Appendix C details the process flow of this transaction.

Aurizon shares

Queensland Treasury Holdings Pty Ltd, a subsidiary of Queensland Treasury, held 54.9 million shares in Aurizon Limited after the privatisation of QR (Queensland Rail) National in 2010. In April 2021, the shares, valued at $206 million, were transferred into the Debt Retirement Fund. There is no net impact on Queensland Treasury’s overall financial statements from this transfer, as these shares were already recorded in its financial statements prior to the transfer.

Appendix C details the process flow of this transaction.

What has happened to the assets?

As mentioned earlier, the Queensland Future Fund Act 2020 created the concept of ‘prescribed’ assets, which must always be held by the state and not sold or transferred into private ownership.

However, the investments transferred into the Debt Retirement Fund during 2020–21 are not prescribed assets, and significant portions of them changed ownership after being placed in the fund, though all of the ownership of Queensland Titles Registry remained with government entities.

This was done to diversify the investments of the Debt Retirement Fund and provide cash for operations.

Several key transactions occurred after the assets were contributed to the fund:

- In May 2021, a portion of the Aurizon shares were sold on the Australian Stock Exchange. This was completed as part of usual trading of investments.

- On the same day the Queensland Titles Registry operations transferred to the Debt Retirement Fund, $2.1 billion was borrowed. This occurred in a company within the Queensland Titles Registry structure to provide liquidity to the fund and support the state’s credit rating.

- The Debt Retirement Fund transferred part of its ownership of the Queensland Titles Registry to other Queensland government funds and entities. In exchange, it received more liquid investments from these entities.

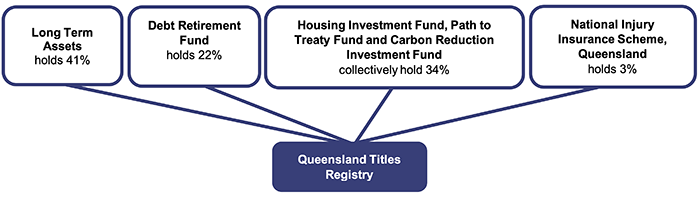

This meant that, as at 30 June 2021, there were four owners of the Queensland Titles Registry, as shown in Figure 2E.

Note: Long Term Assets is the pool of funds held by the government to fund long‑term obligations of the state, including the defined benefit fund.

Compiled by the Queensland Audit Office.

While the indirect owners of the Queensland Titles Registry were all government entities as at 30 June 2021, there is no legislative protection under the Queensland Future Fund Act 2020 or the Queensland Future Fund (Titles Registry) Act 2021 to prevent some or all of the holdings in the Queensland Titles Registry from being sold to private entities. Agreement of all owners is required for any changes in the ownership structure. A change in ownership may also result in tax obligations for the Queensland Titles Registry.

On 30 June 2021, the Debt Retirement Fund held the remaining portion of Aurizon shares and its holding in the Queensland Titles Registry, which was valued at $1.3 billion. The remaining value of the fund was invested across other funds QIC Limited manages, including cash, real estate, and private businesses. Figure 2F outlines the assets of the fund as at 30 June 2021.

Compiled by the Queensland Audit Office.

Achievement of objectives

The 2021–22 state budget announced the objectives the government wanted to achieve through the Queensland Future Fund. Figure 2G outlines assessment of what progress has been made on these objectives to date.

|

Budget objective |

Progress assessment |

|---|---|

|

Provide for debt reduction |

As at 30 June 2021, no debt had been paid down from the Queensland Future Fund, because it had only been operating for a short time. The ratio of net debt held by the government compared to the revenue it generates, however, did decrease due to the creation of the Debt Retirement Fund. |

|

Hold state investments for future growth |

The assets contributed were those formerly held by the state. A number of these have been partially sold, or transferred to other government entities to increase the liquidity of the Debt Retirement Fund. This was allowed as they were not prescribed assets. |

|

Offset state debt to support Queensland’s credit rating |

This will be measurable in late 2021, when the first credit rating (since the fund was established) is issued. |

|

Play a material role in the state’s management of its debt |

This cannot be assessed in the early stages of the Queensland Future Fund. Progress will be measured on this in future years. |

|

Provide a contribution of $7.7 billion to the Debt Retirement Fund as at 30 June 2021 |

This was achieved with the transfer of the operations of the Queensland Titles Registry, Aurizon shares, and a portion of the defined benefit surplus. |

Compiled by the Queensland Audit Office.

Reporting on financial performance

In its 2020–21 annual report, Queensland Treasury presented information on the Queensland Future Fund relating to:

- contributions made into the fund

- the allocation of the investments in the fund as at 30 June 2021

- the accounting policy for ‘Other financial assets’ (which is how Queensland Treasury records the Queensland Future Fund in its financial statements).

Queensland Treasury also provided information on the strategic asset allocation as at 30 June 2021 and provides some information on the governance of the Queensland Future Fund.

In addition, impacts of the future fund arrangements were disclosed across the financial statements of multiple entities, including the:

- Queensland Treasury Corporation, which recorded the value of the future fund investments (managed by QIC within the Debt Retirement Fund) and the financial instrument issued to Queensland Treasury in return for the investments

- Queensland Treasury Holdings, which recorded the transferred Aurizon shares

- Department of Resources, which recorded the assets and liabilities of the transferred Queensland Titles Registry

- Report on State Finances, which recorded the transferred defined benefit surplus, and shows the overall investment in the Debt Retirement Fund and the three funds (the Housing Investment Fund, Path to Treaty Fund and Carbon Reduction Investment Fund) through its reporting of the results of all state entities. This report also provided information on the establishment and funding of the Debt Retirement Fund

- Debt Retirement Trust, which recorded the value of the underlying investments. (These are audited special purpose financial statements prepared by QIC and are not available publicly.)

All of these financial statements need to be considered in order to fully understand the impact of the Queensland Future Fund across government.

To make the overall impact clearer, Queensland Treasury should prepare separate financial statements for the Queensland Future Fund. This would be comparable to the NSW Generations Fund, which is required to provide a separate annual report, including publicly available and audited financial statements for each of the funds it manages.

Separate financial statements would also provide enhanced accountability to parliament and the public if changes occur in the fund that impact on the investments, particularly ownership of the assets contributed to the fund. This will support the Queensland Government’s measure of an ‘open and transparent government’.

Separate financial statements would provide clear and audited disclosure of the Queensland Future Fund and would align to practices in other jurisdictions.

This recommendation was previously raised in our State finances 2020 (Report 15: 2020–21) report and was not accepted. We have re-raised this recommendation based on the transactions within the Queensland Future Fund structure in 2020–21 and the disaggregated information available on these activities.