Overview

State and local government owned water entities provide water throughout Queensland, to households, agriculture, mining, electricity generation, tourism, and manufacturing industries.

Tabled 10 November 2021.

Report on a page

This report summarises the audit results of six entities in Queensland’s water sector: Seqwater, Sunwater, Urban Utilities, Unitywater, Gladstone Area Water Board, and Mount Isa Water Board.

Seqwater is no longer liable for damages from the 2011 South East Queensland floods class action

In February 2021, Sunwater and the Queensland Government agreed to pay $440 million in relation to the 2011 South East Queensland floods class action. Seqwater successfully appealed against the court judgement, which means it is no longer liable to pay damages to the group members of the class action. That decision does not impact on the settlement being paid by Sunwater and the Queensland Government.

Financial statements are reliable

All entities’ financial reports are reliable and comply with relevant laws and standards. They have been prepared in a timely manner and are of good quality.

Weaknesses in information systems continue

We continue to identify weaknesses in the information systems water entities use to prepare financial statements. These weaknesses allowed a cyber breach to occur at one entity and remain undetected for nine months. Entities need to establish stronger processes for monitoring access to systems.

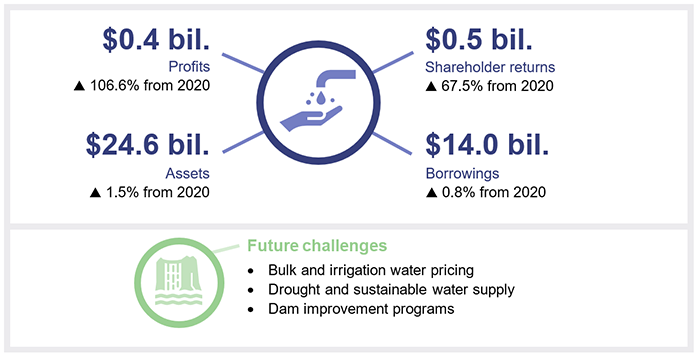

Profits and shareholder returns have increased

Sunwater’s settlement as part of the 2011 South East Queensland floods class action was $80 million lower than it estimated in 2019–20. Previously, Sunwater recognised a liability (and matching expense) of $330 million based on its best estimate of the obligation at that time. The reduced settlement adjusted its profit and the combined profit of the sector. While shareholder returns were higher than in previous financial years, the floods class action adjustment did not flow through to dividends.

However, continuing improvements to assets involving significant infrastructure investment are likely to impact on the sector’s returns to shareholders over the next decade.

Drought, the sustainable supply of water, and dam improvement programs continue to pose challenges

The ongoing drought in Queensland—particularly in the Central and South East regions—highlights that projects that contribute to the reliable provision of an acceptable quality and quantity of water are a priority. The drought increases operating costs, and entities also need to fund projects to make water supply more sustainable.

We are undertaking a performance audit that will provide insights on the Department of Regional Development, Manufacturing and Water’s framework for ensuring dams are managed safely.

Recommendations for entities

Information systems recommendation requiring immediate action

Our only recommendation for the water entities this year is that they address the security of their information systems. This was one of our three recommendations in Water 2020 (Report 9: 2020–21), and has become even more important this year as several entities have introduced new systems and there has been a recent cyber breach in one of the water entities.

We continue to identify significant control weaknesses in the security of information systems. All entities must have strong security practices to protect against fraud or error, and significant reputational damage.

Prior year recommendations addressed

Water entities have taken appropriate action in relation to two of the three recommendations made in our report last year:

- Urban Utilities and Unitywater have improved the timely recognition of donated assets (charges paid by developers through the donation of assets such as water and sewerage infrastructure). Given the time lag between building applications and receiving donated assets, historical issues causing delays in revenue recognition may still happen throughout the year. However, no new issues have been identified that indicate an ongoing underlying risk.

- All entities have implemented appropriate processes to understand complex employee arrangements arising from the interaction of employee contracts with enterprise agreements.

We have included a full list of prior year recommendations and their status in Appendix C.

Reference to comments

In accordance with s.64 of the Auditor-General Act 2009, we provided a copy of this report to relevant entities. In reaching our conclusions, we considered their views and represented them to the extent we deemed relevant and warranted. Any formal responses from the entities are at Appendix A.

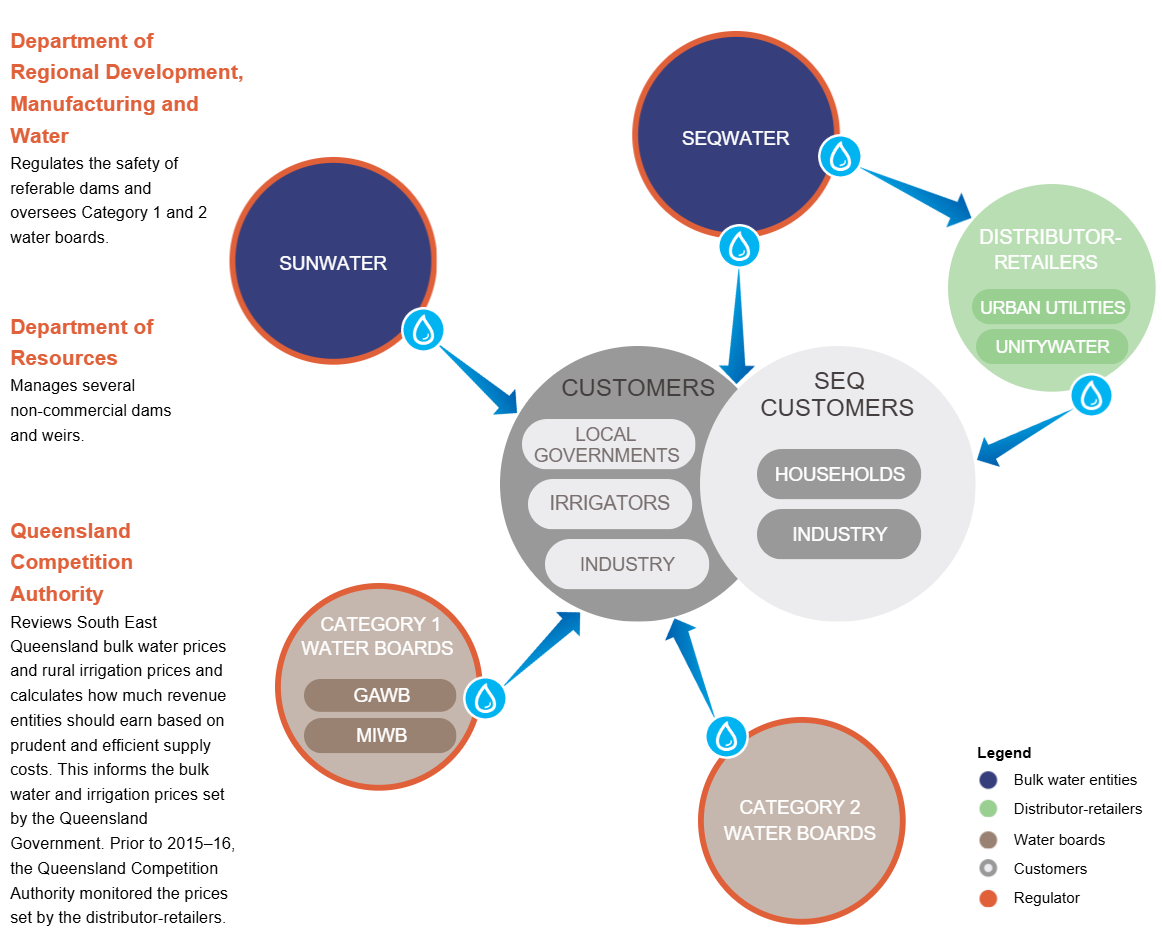

1. Overview of entities in this sector

Notes:

- Distributor-retailers are entities established under the South-East Queensland Water (Distribution and Retail Restructuring) Act 2009 to purchase and distribute water; deliver water and wastewater services; charge customers for relevant services; manage customer enquiries, service requests and complaints; perform functions relating to trade waste and seepage; and perform planning and development assessment functions under the Planning Act 2016.

- A dam is referable if a failure impact assessment demonstrates there would be two or more people at risk if the dam was to fail.

- Bulk water entities are entities that provide bulk water services to water service providers (for example, distributor-retailers, or local governments). Bulk water means a large quantity of water. It is supplied in a wholesale arrangement between water providers, with the recipient then distributing to final customers according to a bulk water supply agreement.

- Seqwater, Sunwater, and the water boards also directly supply water to local governments that operate their own retail businesses. Like distributor-retailers, these local governments on-sell water to households or industries. Local governments are excluded from this report.

- South East Queensland (SEQ) customers refers to household and industry customers in the Brisbane, Ipswich, Somerset, Lockyer Valley, Scenic Rim, Moreton Bay, Sunshine Coast and Noosa council areas.

- Category 1 water boards are for-profit authorities established under the Water Act 2000. GAWB—Gladstone Area Water Board; MIWB—Mount Isa Water Board.

- Category 2 water boards are smaller water authorities and are outside the scope of this report.

Compiled by the Queensland Audit Office.

2. Results of our audits

This chapter provides an overview of our audit opinions for the entities in the water sector. It also evaluates the effectiveness of the systems and processes (internal controls) the entities use to prepare financial statements.

Chapter snapshot

Audit opinion results

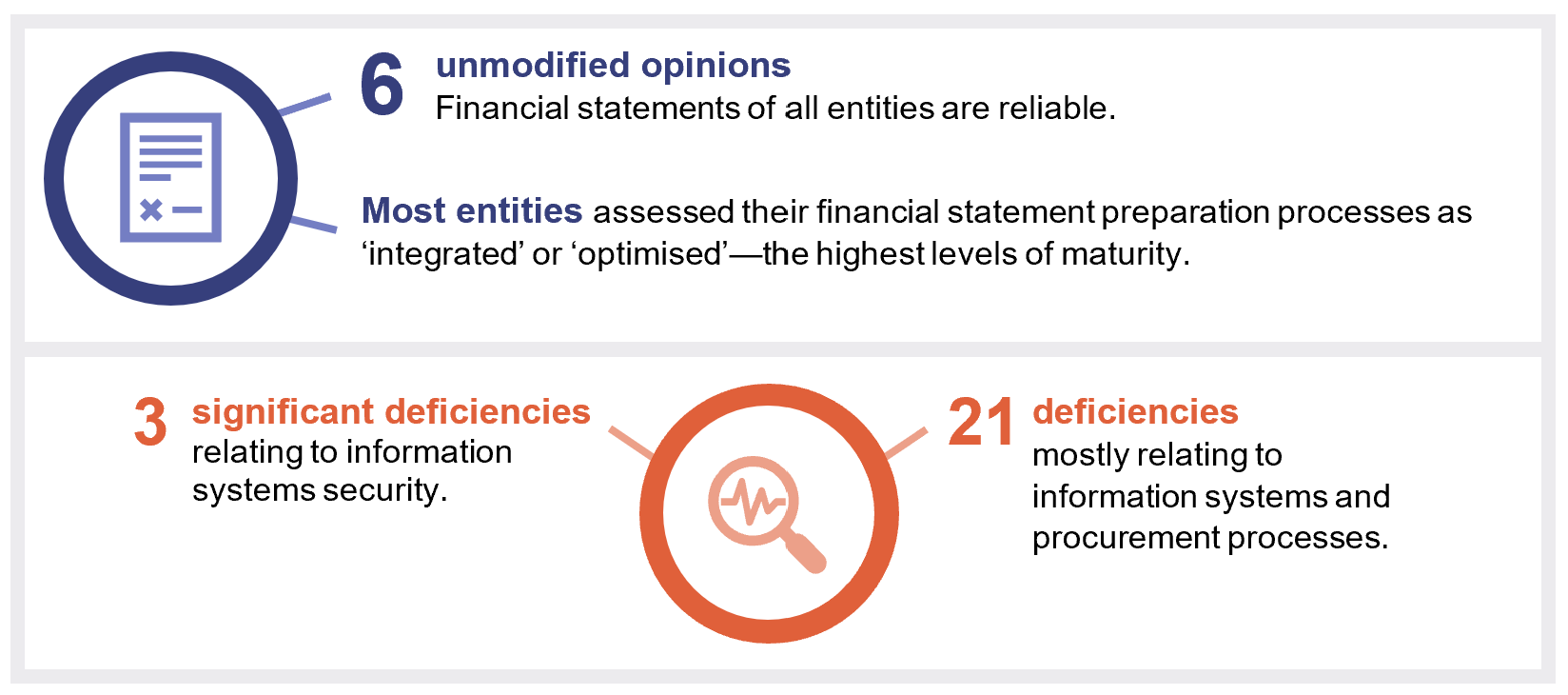

We issued unmodified audit opinions to all six entities, meaning their financial statements can be relied on. Five out of six water entities met their legislative deadline of 31 August 2021. Seqwater’s financial statements were certified on 21 September 2021.

In 2019–20, we qualified our opinion on Seqwater for not recording a liability and matching expense as a result of the unfavourable court judgement relating to the 2011 South East Queensland floods class action.

Seqwater’s successful appeal against the court judgement was announced on 8 September 2021—before its financial statements were published in its annual report. We subsequently issued an unmodified opinion on its 2020–21 financial statements on 21 September 2021 based on this new information. Appendix D provides details about the audit opinions we issued in 2021.

Most water entities have self-assessed their financial statement preparation as ‘integrated’ or ‘optimised’—the highest levels in the Queensland Audit Office’s financial statement preparation maturity model. This means they believe their processes for preparing financial statements are efficient and provide high-quality information in a regular, timely manner. The results of our audits support their assessments.

We express an unmodified opinion when financial statements are prepared in accordance with the relevant legislative requirements and Australian accounting standards.

We express a qualified opinion when financial statements are fairly presented, with the exception of a specified area.

Entities not preparing financial statements

Not all Queensland public sector water entities produce financial statements. Appendix E provides a full list of those who do not, and the reasons why.

Liabilities from the 2011 South East Queensland floods class action

A class action relating to the 2011 South East Queensland floods was brought against Seqwater, Sunwater, and the Queensland Government through the Supreme Court of New South Wales (the Court). A judgement was handed down in favour of the plaintiff in November 2019 and the Court determined the percentage of liability to be allocated between Seqwater (50 per cent), Sunwater (30 per cent) and the Queensland Government (20 per cent) in May 2020. This created a financial obligation to the group members of the class action that could be estimated and was likely to require payment.

A class action is a court proceeding where the claims of a group or ‘class’ of persons are brought by one or a small number of named representatives.

In February 2021, Sunwater and the Queensland Government agreed to pay $440 million, and the Court approved the settlement in May 2021. Sunwater and the Queensland Government have progressed to settling the claims against them, including costs and interest. Sunwater has appropriately recognised a liability, payable in the next 12 months.

In September 2021, the New South Wales Court of Appeal overturned the Court’s November 2019 decision, which had found Seqwater was negligent in relation to the 2011 South East Queensland floods. As a result, Seqwater is no longer liable to pay damages.

This decision has no impact on the settlement agreement approved by the Court in May 2021 in respect to Sunwater and the Queensland Government.

Internal controls are generally effective

We assess whether the internal controls used by entities to prepare financial statements are reliable, and report any deficiencies in their design or operation to management for action. Those simply rated as deficiencies are of lower risk and can be corrected over time. Those rated as significant deficiencies are of higher risk and require immediate action by management.

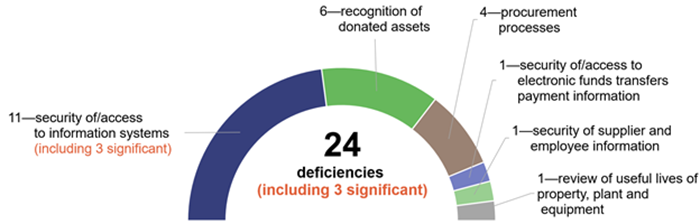

Overall, we found the internal controls the water sector entities have in place to ensure reliable financial reporting are generally effective, but they can be improved. One entity’s control environment was assessed as ineffective due to three significant deficiencies identified during the audit.

In addition to these, we also reported 21 deficiencies in internal controls across the sector this year. Figure 2A shows the types of deficiencies we identified.

Compiled by the Queensland Audit Office.

We have received responses from each entity on planned corrective action for the internal control issues raised. We are satisfied with the responses and proposed implementation time frames. However, we continue to identify significant control weaknesses in the security of information systems. This is a critical issue for water sector entities and should be addressed as soon as possible.

Immediate action needs to be taken to address ongoing security weaknesses in information systems

Water entities rely on information technology systems to operate their businesses and prepare financial statements. They must have strong controls over who has access to the systems and the information in them. Weaknesses in information technology controls increase the risk of undetected errors or potential financial loss, including fraud.

In our water report last year, we found that the security of information systems was the most common internal control weakness across the public sector. We made the same recommendation across all our sector reports for entities to strengthen the security of their information systems.

Not all the water entities have fully addressed this recommendation. We identified control weaknesses in information system security at three of the six entities this year. Appendix C provides the full recommendation and status as at 30 June 2021.

Weaknesses in user access to systems

Monitoring access to systems in a timely manner is essential. Any unauthorised access could result in fraud or error and significant reputational damage. For one entity, we raised three significant deficiencies relating to management of user access across multiple systems (financial, invoicing, and payroll). Entities should only assign employees the minimum access required to perform their jobs.

Security weaknesses exposed by a cyber breach

A cyber breach (between August 2020 and May 2021) resulting in unauthorised access to an entity’s web server was identified during the year. Threat actors (those conducting malicious activities against entities) targeted an older and more vulnerable version of the system. The web server that stores customer information contained suspicious files that increased visitor traffic to an online video platform. This did not result in lost customer or financial information. The entity implemented a number of measures to address the breach, including updating software, using stronger password practices, and monitoring incoming and outgoing network traffic.

As entities use more cloud-based services (which provide remote access to systems), cyber risk vulnerabilities and exposures must be continuously assessed. Entities need to make sure their users are aware of their responsibilities in managing cyber risks. We have previously presented two reports to parliament on this—Managing cyber security risks (Report 3: 2019–20) and Security of critical water infrastructure (Report 19: 2016–17).

Improve timely recognition of donated assets

Distributor-retailers collect infrastructure charges (developer contributions) from developers. Developer contributions are settled through cash contributions or donated assets (for example, water and sewerage infrastructure). In 2019–20, we reported on control weaknesses affecting the timely recognition of donated assets.

During 2020–21, distributor-retailers undertook an independent review to amend data inconsistencies. As a result, weekly compliance checks of all donated assets were implemented to ensure completeness and accuracy of data. Entities will ensure new controls are operating effectively. Processes are also in place to identify historical issues (similar to those identified previously) that may persist in future years. Trends in developer contributions and building approvals are shown in Appendix F.

Assessment tools for internal controls

We are developing new assessment tools for internal controls relevant to public sector entities. They will provide the entities with greater insight into the strength of their internal control processes.

These tools focus on asset management, change management, culture, governance, grants management, information systems, monitoring, procure-to-pay (the whole procurement process), record keeping, and risk management.

We are currently consulting with our clients on these tools and intend to begin using them in our audits from 2021–22. Our reporting on internal control deficiencies will not change.

3. Financial results and challenges

This chapter analyses the key financial results and challenges faced by the water sector.

Chapter snapshot

Rising profits and shareholder returns

The water sector’s profits increased by $234.7 million (106.6 per cent) in 2020–21. The largest impact was an adjustment to Sunwater’s profit in relation to the 2011 South East Queensland floods class action. The settlement between Sunwater and group members of the class action was $80 million less than originally estimated in 2019–20.

Seqwater successfully appealed against the original judgement. The New South Wales Court of Appeal’s decision on this, in September 2021, means Seqwater is no longer required to pay damages to the class action members. This decision did not have an impact on Seqwater’s results for 2020–21.

Seqwater did not pay a dividend in 2020–21 despite reporting a profit. From 2021–22, it will start repaying principal and interest on its debt to the Queensland Government.

Shareholder returns were higher than in the prior year, due to the sector’s increased profits. The sector’s total shareholder returns of $497.2 million were made up of dividends (a share of profits paid to Queensland Government shareholders), participation returns (a portion of a distributor-retailer’s profits paid to participating local governments), and income tax equivalents (which are paid by commercial operations in government instead of tax and include deferred tax components). Details on financial flows to and from government are provided in Appendix J.

Notes:

- Profit is after income tax equivalents.

- Shareholder returns are made up of dividends (a share of profits paid to Queensland Government shareholders), participation returns (a portion of a distributor-retailer’s profits paid to participating local governments), and income tax equivalents (which are paid by commercial operations in government instead of tax and include deferred tax components).

- *Shareholder returns have moved from those reported last year due to prior period adjustments for donated assets.

Compiled by the Queensland Audit Office from water sector entities’ financial reports.

Bulk and irrigation water pricing

In response to COVID-19, the Queensland Government decided to defer the Queensland Competition Authority's (QCA) review of the South East Queensland bulk water (wholesale) prices to 2021–22. This resulted in the bulk water price for 2020–21 being rolled forward for one additional year (2021–22), with the government recently directing the same 3.5 per cent increase that was applied in 2020–21.

The QCA is currently reviewing Seqwater’s bulk water pricing practices, and will recommend bulk water prices to apply from 1 July 2022 to 30 June 2026. The QCA expects to recommend prices to the Queensland Government (in March 2022) that will allow Seqwater:

- sufficient revenue to recover prudent and efficient costs of providing bulk water supply services

- repay its price path debt by 2027–28.

The government continues to pay community service obligation payments to compensate Sunwater and Seqwater where the government has set irrigation prices below the cost of supply. This includes where prices are below costs as a result of the 15 per cent discount due to the government’s 2020 election commitment to provide discounts on irrigation prices. Discounts on irrigation water prices continue to 2023–24.

Community service obligation payments for 2020–21 amounted to $19.7 million (2019–20: $9.7 million).

Price path is a 20-year period established by the Queensland Government in 2008 for the annual increase in bulk water prices to gradually repay debt and achieve a common bulk water price across all South East Queensland councils.

Price path debt was incurred when bulk water prices charged were less than the cost of treatment and supply—water cost more than was charged to customers.

Irrigation water is the supply of water or drainage services for irrigation of crops or pastures.

Community service obligations are government payments to ‘for-profit’ entities to provide services that are not sustainable otherwise.

Drought and sustainable water supply

Queensland continues to experience extreme weather conditions, with 34 councils (64.7 per cent of the state) fully drought-declared. Prolonged drought has led to reduced water storage levels, increased operational costs, and the need for increased capital investment in water security projects (which contribute to the sustainable provision of an acceptable quality and quantity of water). Details of drought‑declared areas are provided in Appendix G.

Infrastructure projects to ensure sustainable water supply

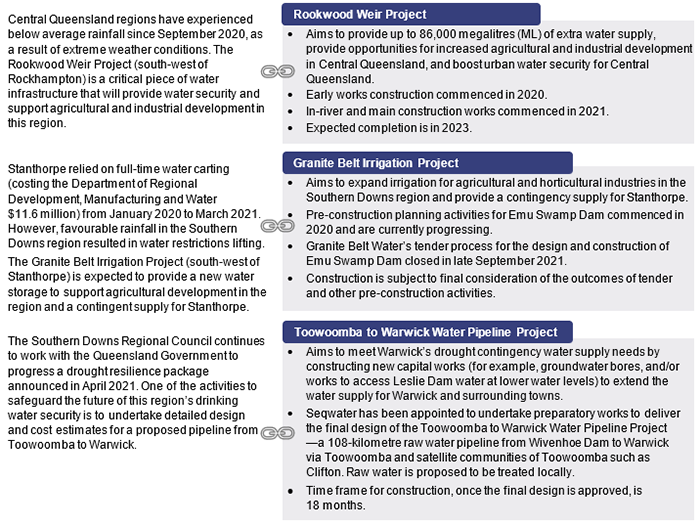

The sector has several projects underway to address the issue of water supply in drought-declared areas across Queensland. For communities that are experiencing severe drought, interim solutions are in place to help them receive continuous supplies of water.

For example, several off-grid (not fully dependent on public utilities) communities in the Scenic Rim, Somerset, and Moreton Bay regions entered into various levels of water restrictions in October 2020. All except a community in the Moreton Bay region (Dayboro) came off restrictions following rain in mid-December 2020. Dayboro required periodic carting of water to maintain supply until early February 2021. In March 2021, Rockhampton Regional Council started carting 20 trucks of water from Gracemere to Mount Morgan each day. This is equivalent to about 160 litres per person per day. The projects shown in Figure 3B are expected to contribute to long-term water security for drought-declared regions.

Compiled by the Queensland Audit Office from Department of State Development, Infrastructure, Local Government and Planning and Department of Regional Development, Manufacturing and Water information.

All other long-term water security projects are in the early stages of planning or feasibility studies (which take technical, environmental, and economic assessments into account). These projects are important to ensuring sustainable water supply during drought, but they will take time and resources to plan and construct.

Maintaining water supply in South East Queensland

Seqwater’s South East Queensland's Water Security Program 2016–2046 includes drought responses that are triggered when the combined total of the region’s 12 major dams (the water grid) reduces to predetermined levels. The region’s 60 per cent drought response trigger has been reached twice over the past two years (November 2019 and September 2020). South East Queensland’s water grid is currently at 60.2 per cent (at 30 June 2021), with medium-level water restrictions due to come into place when the water grid level falls to 50 per cent. At 60 per cent, the Gold Coast Desalination Plant goes to full production, while recommissioning of the Western Corridor Recycled Water Scheme commences.

Figure 3C outlines the annual maintenance and operating costs for the water security programs along with how much water they have contributed to the South East Queensland water grid.

|

Gold Coast |

|

Western Corridor |

Note: ML—Megalitres.

Compiled by the Queensland Audit Office from Seqwater data.

The Western Corridor Recycled Water Scheme—a water recycling scheme that treats wastewater effluent from Brisbane and Ipswich at three water treatment plants—remained in ‘care and maintenance’ mode (which means it was not used at full capacity) throughout 2020–21. Purified, recycled water from the scheme was used in power stations in place of water from dams. Its assets become fully operational when the region’s water grid level falls to 40 per cent, subject to required government and regulatory approvals.

Since November 2019, Seqwater has maximised production from the Gold Coast Desalination Plant to supplement the water grid during a period of extended drought.

Manufactured water assets relate to climate-resilient water infrastructure assets.

Dam improvement programs

Each dam owner is responsible for improvements to their dam/s and must ensure they manage safety risks in accordance with the provisions of the Water Supply (Safety and Reliability) Act 2008 (the Act). We are undertaking a performance audit that will provide insights on the Department of Regional Development, Manufacturing and Water’s framework for ensuring dams are managed safely.

Dam owners regularly monitor and assess their dams to maintain public safety and to secure water supply. The department conducts desktop assessments of the reports and notifications to ensure owners are complying with the requirements of the Act. The significant cost of dam improvement programs continues to be a challenge to entities, and the full extent of the cost is usually unknown until actual works commence. Until then, estimates could vary. The costs are funded through additional borrowings, funding from the state or federal government, and current and future water prices.

As an example of the complexity of dam improvement projects, Lake Macdonald Dam (Six Mile Creek), which provides drinking water storage for the Noosa region, requires an upgrade to meet the standards and performance requirements of dam safety regulations. Improvements were originally scheduled to begin in 2020–21. During the procurement stage in December 2020, it became known that the project costs would be greater than the approved $127 million budget (based on a detailed design completed in late 2019). The potential cost increase is due to a more thorough understanding of the project, based on:

- the detailed design of the dam wall structures

- the construction complexity

- additional risk mitigation activities required due to approval conditions.

Seqwater is reassessing the upgrade options to ensure dam safety, water security, and environmental and community objectives are met. A decision is expected to be made by the board in 2021–22. Completion of the upgrade is required by 2035.

The sector’s returns to shareholders are likely to be impacted as asset improvement programs continue to involve significant infrastructure investments.

A dam improvement program is a program to upgrade a portfolio of referable dams to meet industry recommended standards. A dam is referable if a failure impact assessment demonstrates there would be two or more people at risk if the dam was to fail.

2021 water dashboard

This Queensland Audit Office interactive map of Queensland allows you to explore the financial performance of the state's water entities, and view storage levels, the number of dams, and drought declared areas across the state. You can find information on your water services by typing your address into the search bar or clicking on your local council.